Sustainability dimensions in goods movement

Sustainability dimensions in goods movement

The section “Sustainability dimensions in goods

movement” provides you with an overview of the three pillars of sustainability

– society, environment and economy – and its importance for goods movement.

1. Introduction

In this section you will learn more about the sustainability of goods movement. Because all kind of transport has a sustainable impact, we will show you in this section, what measures can be taken to reduce this negative impact. After the three pillars of sustainability have been explained, the structure of the conceptual system model and its goods, movables, infrastructure and facilities and their impact on sustainability will be presented.

Political environment for sustainability

In the past, there were only a few people who were concerned with the preservation of the earth. In Germany, this role has mainly been assumed by the state since the 1970s. In recent decades, the European Union (EU) has enforced stricter policies and laws than was the case in Germany. At international level, the institutions have now agreed on a large number of ecological and social standards which are introduced in this section. The political room for action relates mainly to the formulation of limit values, the enforcement of taxes and the linking of the allocation of public funds to ecological and social standards. The EU-green paper, stated by the European Commission in 2013, defined a 2030 framework for climate and energy policies. It integrates different policy objectives such as reducing greenhouse gas (GHG) emissions, securing energy supply and supporting growth, competitiveness and jobs through a high technology, cost effective and resource efficient approach.The three pillars of sustainability

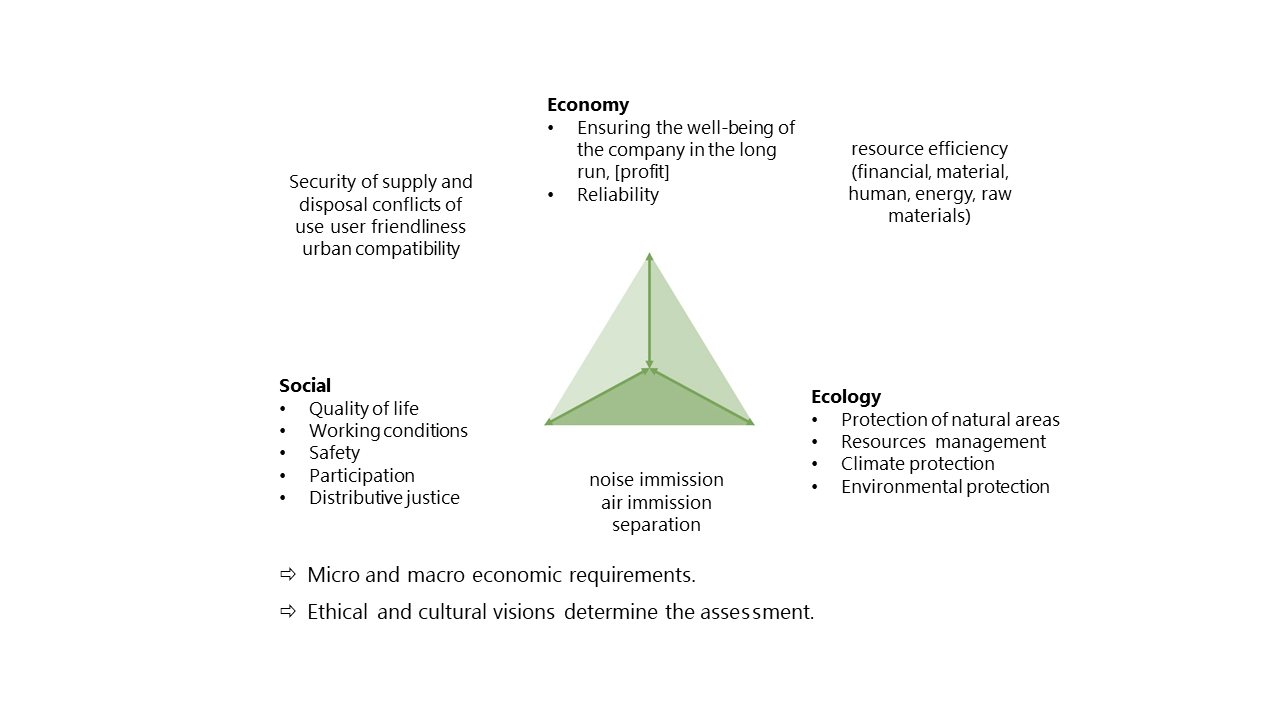

The three pillars of sustainability – society, environment and economy – provide a solution-oriented framework to help companies tackle complicated sustainability issues. The included aspects of the three dimensions are shown in the following figure.Social sustainability includes environmental justice, human health, resource security, and education. While the ecological pillar focuses the well-being of the environment including water quality, air quality, and reduction of environmental stressors (e.g. greenhouse gas emissions), economic sustainability focuses the well-being of the company including job creation, profitability, and proper accounting of ecosystem services for optimal cost-benefit analyses.

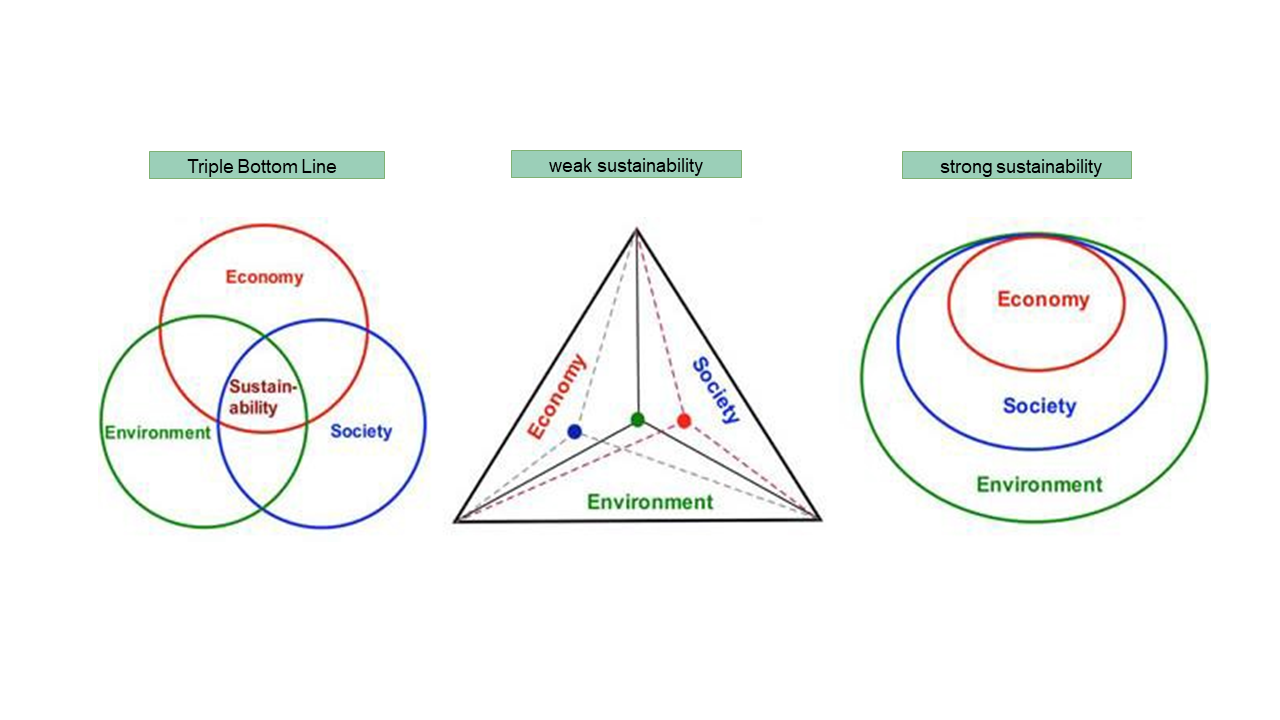

Triple Bottom Line

There are different perspectives on the dimensions of sustainability and how they relate to the limits of the planet’s environment. The Triple Bottom Line is a concept for sustainable management. The economic principle is supplemented by ecological and social factors. This means that companies should act in such a way that they offset or at least minimize their ecological and social impact. By taking social and ecological aspects into account, a company offsets its ecological and social footprint and thus contributes to sustainability. This also ensures long-term economic success. An exclusive focus on profit maximization harms the company in the long term, as social and ecological factors are neglected.

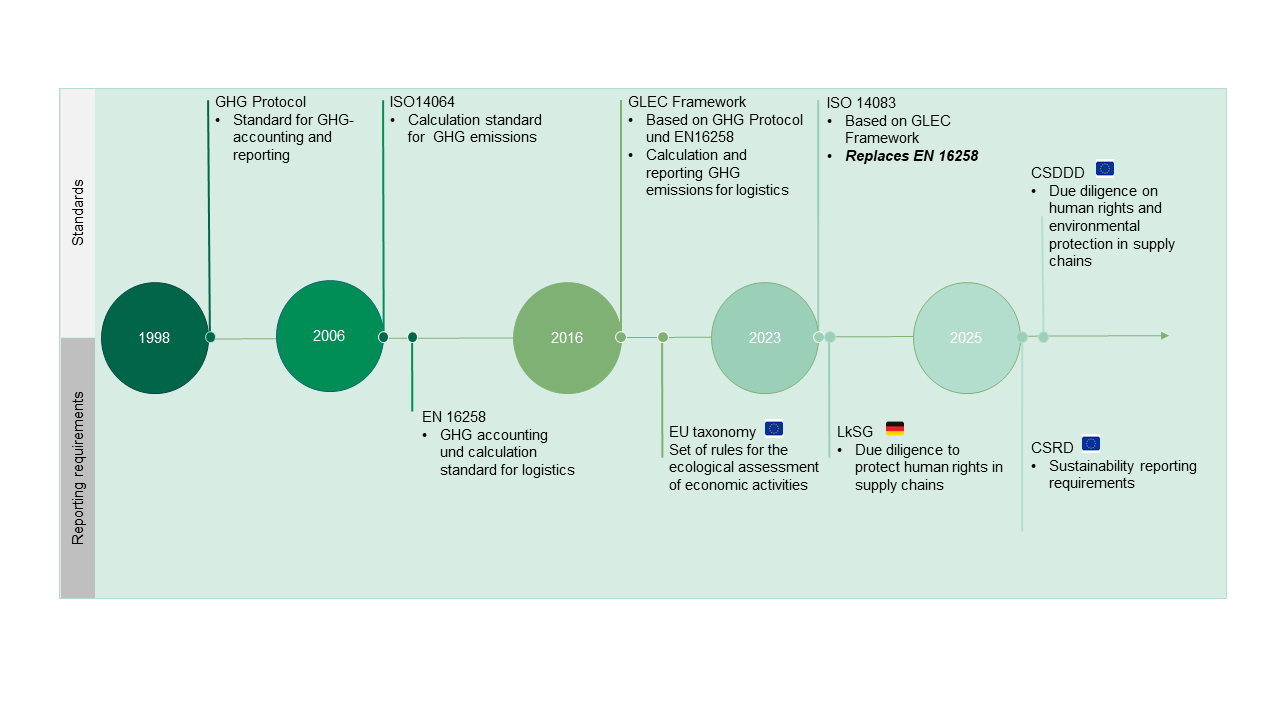

Non-financial reporting requirements and standards in the area of logistics

The relevance of sustainability reporting continues to increase due to new regulations. The following figure “Milestones to more sustainability in logistics” shows you important standards and reporting requirements for logistics from the past and coming years. The Greenhouse Gas Protocol established the first standard for greenhouse gas accounting and reporting in 1998. Several standards and reporting requirements were defined in the following years. The calculation standard for GHG emissions ISO 14064 from 2006 was followed in 2013 by the reporting requirement DIN EN 16258, which is specifically aimed at logistics companies. These regulations formed the basis for the GLEC framework, a guideline for logistics companies for calculating and reporting their greenhouse gas emissions. ISO 14083 from 2023 is based on this framework and replaces DIN EN 16258. The new standard covers all lifting activities and refrigerant losses. It covers the entire transport chain and all relevant modes of transport (for both passenger and freight transport). It also includes direct emissions as well as upstream emissions from the provision of fuel and electricity. Since 2024, the CSRD (Corporate Sustainability Reporting Directive) and the CSDDD (Corporate Sustainability Due Diligence Directive) are into force in the EU member states; the two directives contain the requirements for sustainability reporting (CSRD) and due diligence with regard to human rights and environmental protection in supply chains.

With the growing importance of sustainability due to for example the climate change or politic regulations., the sustainable impact on companies has also increased. The following aspects must be considered in this context:

Growing diversity of topics: Increasing demands on management approaches and data scope

Increasing data requirements: Higher granularity and quality of disclosed data

Greater need for integration: between functions and processes

Greater investor requirements: on information needs, management quality and resilience

One big milestone in the reporting requirements for companies is the Corporate Sustainability Reporting Directive (CSRD). In the following all the relevant aspects concerning the CSRD will be explained to you.

Corporate Sustainability Reporting Directive (CSRD)

The Corporate Sustainability Reporting Directive (CSRD) is the EU directive on corporate sustainability reporting. With this directive large and listed companies are required to publish regular annual reports on their social and environmental risks and explain how their activities affect people and the environment. This affects

- for financial years beginning on or after 1 January 2024: public interest entities with more than 500 employees

- for financial years beginning on or after 1 January 2025: all other large companies under accounting law

- for financial years beginning on or after 1 January 2026: capital market-oriented SMEs, unless they make use of the option to defer until 2028

With the implementation of the CSRD in January 2023, over 50,000 organisations worldwide are obliged to disclose details of their Environmental, Social and Corporate Governance (ESG) practices. In general, this information should help investors, civil society organisations, consumers and other stakeholders to assess the sustainability performance of companies.

CSRD reporting areas and key requirements

Reporting area 1: General requirements and disclosures

Reporting area 2: Environmental

- Climate change

- Pollution

- Water and marine resources

- Biodiversity and ecosystems

- Resource use and circular economy

Reporting area 3: Social

- Own workers

- Worker in the value chain

- Affected communities

- Consumer and end-user

Reporting area 4: Governance

- Business conduct

Read more about CSRD: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:32022L2464

In the following, you will be introduced to some other theories, agreements and standards in the concept of sustainability that have been developed over the years.

Limits to Growth

The statements in the book build on research conducted at Massachusetts Institute of Technology (MIT) on the so-called “world model”, which uses system dynamic modelling. The target group of the report was primarily political decision-makers. The 30-Year Update was published in 2004.

Concept of Sustainable Development (Brundtland-Commission of the EU)

The World Commission on Environment and Development published the Brundtland Report (also called Our Common Future) in 1987, which introduced the concept of sustainable development as follows:“Sustainable development is development that meets the needs of the present without compromising the ability of future generations to meet their own needs. “

"[...] sustainable development is [...] a process of change in which the exploitation of resources, the direction of investments, the orientation of technological development, and institutional change are made consistent with the future as well as present needs.

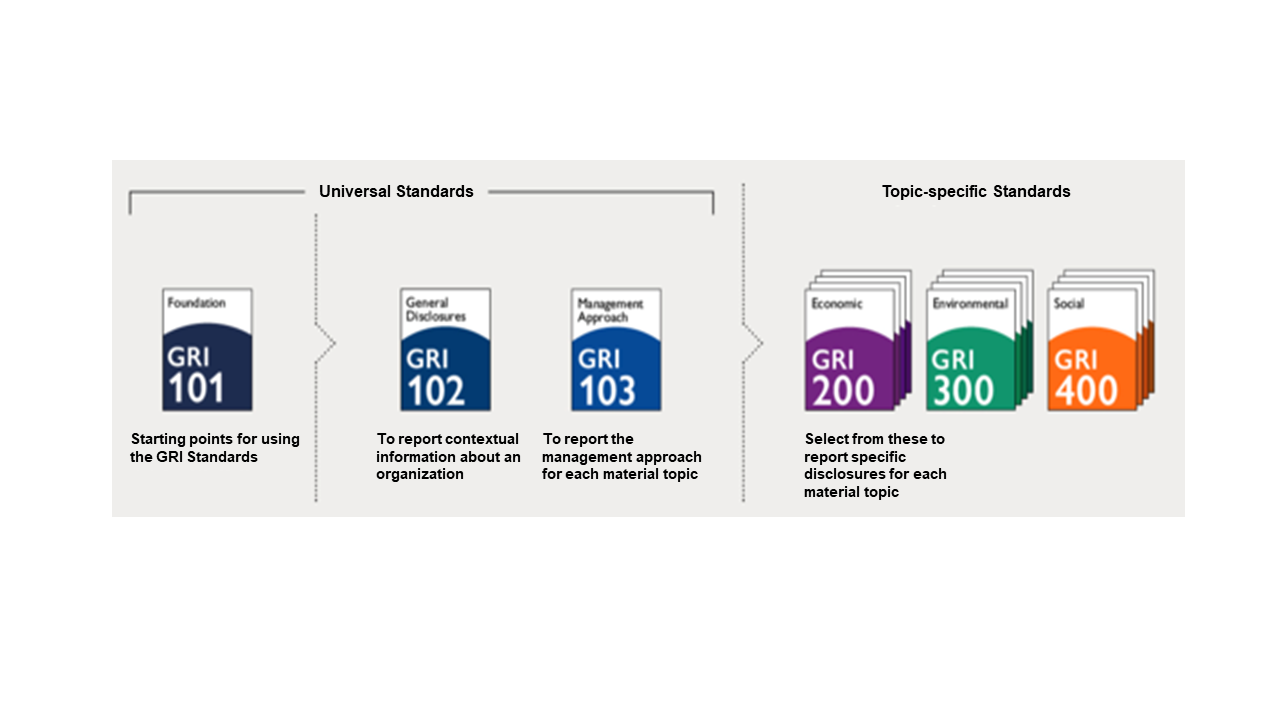

Global Report Initiative (GRI)

The GRI was formed with the support of the United Nations Environment Programme (UNEP) in 1997 and provided the first global standards for sustainability reporting on a range of economic, environmental and social impacts. The GRI Sector Program, which was approved by the Global Sustainability Standards Board (GSSB) on 7 February 2019, is a new program in which standards will be developed that are specific to certain sectors. Those GRI Sector Standards will identify and describe a sector’s impacts and stakeholder concerns from a sustainable development perspective.

If you want to learn more about the current status of the GRI Sector Program, check this website: https://www.globalreporting.org/standards/sector-program/

The Ten Principles of United Nations Global Compact

The United Nations Global Compact defined in 2004 ten principles that provide companies strategies, policies and procedures to follow their sustainable responsibilities and setting the stage for long-term success. The areas of responsibility are human rights, labour, environment and anti-corruption.Human Rights

Principle 2: make sure that they are not complicit in human rights abuses.

Labour

Principle 4: the elimination of all forms of forced and compulsory labour;

Principle 5: the effective abolition of child labour; and

Principle 6: the elimination of discrimination in employment and occupation.

Environment

Principle 8: undertake initiatives to promote environmental responsibility; and

Principle 9: encourage the development and diffusion of environmentally friendly technologies.

Anti-Corruption

Sustainable Development Goals (SDG) (United Nations)

In 2015 the United Nations General Assembly defined the SDGs. It is planned to achieve all the 17 goals by 2030. They should demonstrate a “blueprint to achieve a better and more sustainable future for all.” Furthermore, the goals are defined to address the global challenges and are related to poverty, inequality, climate change, environmental degradation, peace and justice.

Read more about the individual goals: https://www.undp.org/sustainable-development-goals

After this overview of the evolution of sustainability, the following sections will introduce the different dimensions (social, ecological and economic) and show their influence on the movement of goods.

Sources

Bundesministerium für Arbeit und Soziales (2024): Corporate Sustainability Reporting Directive (CSRD). URL: https://www.csr-in-deutschland.de/DE/CSR-Allgemein/CSR-Politik/CSR-in-der-EU/Corporate-Sustainability-Reporting-Directive/corporate-sustainability-reporting-directive-art.html (last access 23.05.2024).

Elkington (1994): Towards the Sustainable Corporation: Win-Win-Win Business Strategies for Sustainable Development. California Management Review, 36, 90-100. http://dx.doi.org/10.2307/41165746

European Commission (2013): Green Paper - A 2030 framework for climate and energy policies. URL: https://eur-lex.europa.eu/LexUriServ/LexUriServ.do?uri=COM:2013:0169:FIN:en:PDF (last access 30.05.2024)

Global Sustainability Standards Board (GSSB) (2021): GRI Standards. URL: https://www.globalreporting.org/standards/ (last access 30.05.2024)

Institut für ökologische Wirtschaftsforschung und future e. V. – verantwortung unternehmen (Hrsg.) (2021): CSR Reporting in Deutschland 2021. URL: https://www.ioew.de/fileadmin/user_upload/BILDER_und_Downloaddateien/Header-Bilder/Publikationen/Ranking_Nachhaltigkeitsberichte_2021_Ergebnisbericht_1.pdf (last access 23.05.2024).

United Nations Global Compact (2020): The Ten Principles the UN Global Compact. URL: https://unglobalcompact.org/what-is-gc/mission/principles (last access 23.05.2024).

United Nations (1987): Brundtland Report. URL: https://www.are.admin.ch/are/en/home/media/publications/sustainable-development/brundtland-report.html (last access 27.05.2024).

United Nations (2015): Transforming our world: The 2030 Agenda for sustainable development. URL: https://sustainabledevelopment.un.org/content/documents/21252030%20Agenda%20for%20Sustainable%20Development%20web.pdf (last access: 30.05.2024)

United Nations (2023): Sustainable Development Goals, Guidelines for the use oft he SDG Logo. URL: https://www.un.org/sustainabledevelopment/wp-content/uploads/2023/09/E_SDG_Guidelines_Sep20238.pdf (last access: 30.05.2023)

Volker Hauff (Hrsg.) (1987): Unsere gemeinsame Zukunft. Der Brundtland-Bericht der Weltkommission für Umwelt und Entwicklung. Greven.

Wu (2013): The problems of weak sustainability and associated indicators. URL: https://www.researchgate.net/figure/From-Wu-2013-Illustration-of-the-triple-bottom-line-definition-of-sustainability-a_fig1_292346996 (last access 23.05.2024).