Sustainability dimensions in goods movement

| Website: | Hamburg Open Online University |

| Kurs: | MoGoLo - Mobility of Goods and Logistics Systems |

| Buch: | Sustainability dimensions in goods movement |

| Gedruckt von: | Gast |

| Datum: | Sonntag, 26. Juli 2026, 19:00 |

Beschreibung

The section “Sustainability dimensions in goods

movement” provides you with an overview of the three pillars of sustainability

– society, environment and economy – and its importance for goods movement.

1. Introduction

In this section you will learn more about the sustainability of goods movement. Because all kind of transport has a sustainable impact, we will show you in this section, what measures can be taken to reduce this negative impact. After the three pillars of sustainability have been explained, the structure of the conceptual system model and its goods, movables, infrastructure and facilities and their impact on sustainability will be presented.

Political environment for sustainability

In the past, there were only a few people who were concerned with the preservation of the earth. In Germany, this role has mainly been assumed by the state since the 1970s. In recent decades, the European Union (EU) has enforced stricter policies and laws than was the case in Germany. At international level, the institutions have now agreed on a large number of ecological and social standards which are introduced in this section. The political room for action relates mainly to the formulation of limit values, the enforcement of taxes and the linking of the allocation of public funds to ecological and social standards. The EU-green paper, stated by the European Commission in 2013, defined a 2030 framework for climate and energy policies. It integrates different policy objectives such as reducing greenhouse gas (GHG) emissions, securing energy supply and supporting growth, competitiveness and jobs through a high technology, cost effective and resource efficient approach.The three pillars of sustainability

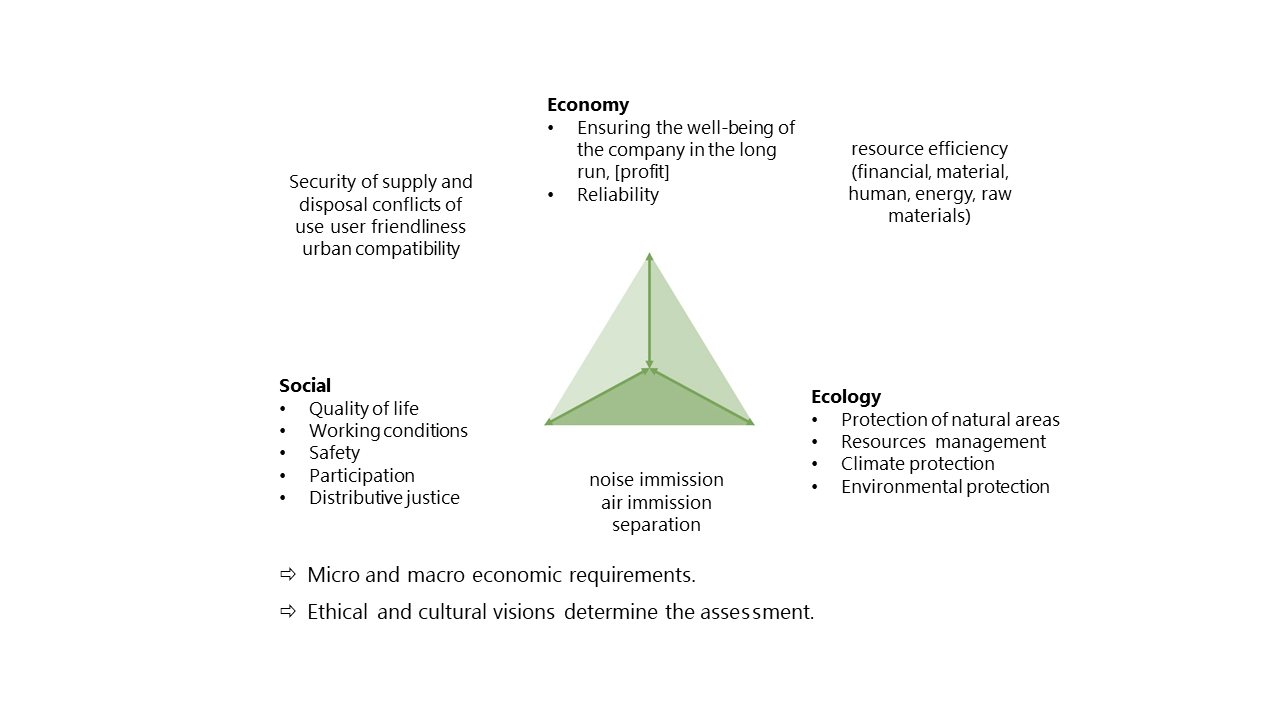

The three pillars of sustainability – society, environment and economy – provide a solution-oriented framework to help companies tackle complicated sustainability issues. The included aspects of the three dimensions are shown in the following figure.Social sustainability includes environmental justice, human health, resource security, and education. While the ecological pillar focuses the well-being of the environment including water quality, air quality, and reduction of environmental stressors (e.g. greenhouse gas emissions), economic sustainability focuses the well-being of the company including job creation, profitability, and proper accounting of ecosystem services for optimal cost-benefit analyses.

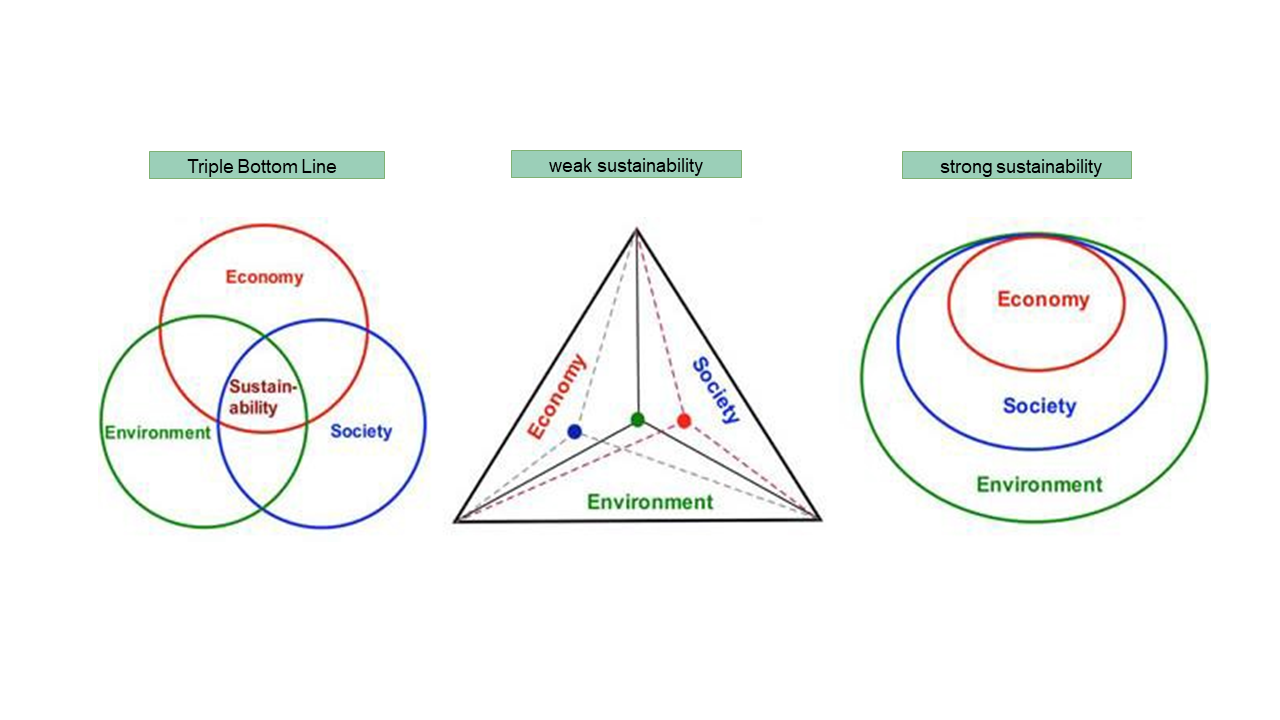

Triple Bottom Line

There are different perspectives on the dimensions of sustainability and how they relate to the limits of the planet’s environment. The Triple Bottom Line is a concept for sustainable management. The economic principle is supplemented by ecological and social factors. This means that companies should act in such a way that they offset or at least minimize their ecological and social impact. By taking social and ecological aspects into account, a company offsets its ecological and social footprint and thus contributes to sustainability. This also ensures long-term economic success. An exclusive focus on profit maximization harms the company in the long term, as social and ecological factors are neglected.

Non-financial reporting requirements and standards in the area of logistics

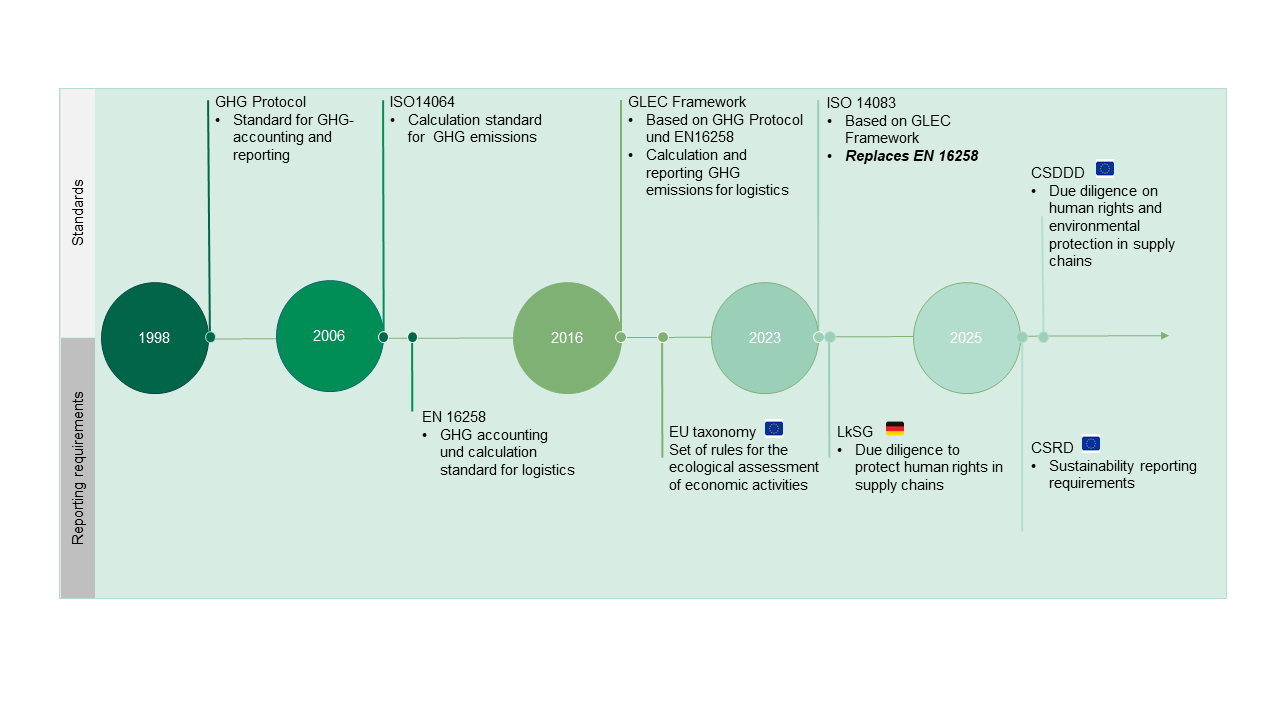

The relevance of sustainability reporting continues to increase due to new regulations. The following figure “Milestones to more sustainability in logistics” shows you important standards and reporting requirements for logistics from the past and coming years. The Greenhouse Gas Protocol established the first standard for greenhouse gas accounting and reporting in 1998. Several standards and reporting requirements were defined in the following years. The calculation standard for GHG emissions ISO 14064 from 2006 was followed in 2013 by the reporting requirement DIN EN 16258, which is specifically aimed at logistics companies. These regulations formed the basis for the GLEC framework, a guideline for logistics companies for calculating and reporting their greenhouse gas emissions. ISO 14083 from 2023 is based on this framework and replaces DIN EN 16258. The new standard covers all lifting activities and refrigerant losses. It covers the entire transport chain and all relevant modes of transport (for both passenger and freight transport). It also includes direct emissions as well as upstream emissions from the provision of fuel and electricity. Since 2024, the CSRD (Corporate Sustainability Reporting Directive) and the CSDDD (Corporate Sustainability Due Diligence Directive) are into force in the EU member states; the two directives contain the requirements for sustainability reporting (CSRD) and due diligence with regard to human rights and environmental protection in supply chains.

With the growing importance of sustainability due to for example the climate change or politic regulations., the sustainable impact on companies has also increased. The following aspects must be considered in this context:

Growing diversity of topics: Increasing demands on management approaches and data scope

Increasing data requirements: Higher granularity and quality of disclosed data

Greater need for integration: between functions and processes

Greater investor requirements: on information needs, management quality and resilience

One big milestone in the reporting requirements for companies is the Corporate Sustainability Reporting Directive (CSRD). In the following all the relevant aspects concerning the CSRD will be explained to you.

Corporate Sustainability Reporting Directive (CSRD)

The Corporate Sustainability Reporting Directive (CSRD) is the EU directive on corporate sustainability reporting. With this directive large and listed companies are required to publish regular annual reports on their social and environmental risks and explain how their activities affect people and the environment. This affects

- for financial years beginning on or after 1 January 2024: public interest entities with more than 500 employees

- for financial years beginning on or after 1 January 2025: all other large companies under accounting law

- for financial years beginning on or after 1 January 2026: capital market-oriented SMEs, unless they make use of the option to defer until 2028

With the implementation of the CSRD in January 2023, over 50,000 organisations worldwide are obliged to disclose details of their Environmental, Social and Corporate Governance (ESG) practices. In general, this information should help investors, civil society organisations, consumers and other stakeholders to assess the sustainability performance of companies.

CSRD reporting areas and key requirements

Reporting area 1: General requirements and disclosures

Reporting area 2: Environmental

- Climate change

- Pollution

- Water and marine resources

- Biodiversity and ecosystems

- Resource use and circular economy

Reporting area 3: Social

- Own workers

- Worker in the value chain

- Affected communities

- Consumer and end-user

Reporting area 4: Governance

- Business conduct

Read more about CSRD: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:32022L2464

In the following, you will be introduced to some other theories, agreements and standards in the concept of sustainability that have been developed over the years.

Limits to Growth

The statements in the book build on research conducted at Massachusetts Institute of Technology (MIT) on the so-called “world model”, which uses system dynamic modelling. The target group of the report was primarily political decision-makers. The 30-Year Update was published in 2004.

Concept of Sustainable Development (Brundtland-Commission of the EU)

The World Commission on Environment and Development published the Brundtland Report (also called Our Common Future) in 1987, which introduced the concept of sustainable development as follows:“Sustainable development is development that meets the needs of the present without compromising the ability of future generations to meet their own needs. “

"[...] sustainable development is [...] a process of change in which the exploitation of resources, the direction of investments, the orientation of technological development, and institutional change are made consistent with the future as well as present needs.

Global Report Initiative (GRI)

The GRI was formed with the support of the United Nations Environment Programme (UNEP) in 1997 and provided the first global standards for sustainability reporting on a range of economic, environmental and social impacts. The GRI Sector Program, which was approved by the Global Sustainability Standards Board (GSSB) on 7 February 2019, is a new program in which standards will be developed that are specific to certain sectors. Those GRI Sector Standards will identify and describe a sector’s impacts and stakeholder concerns from a sustainable development perspective.

If you want to learn more about the current status of the GRI Sector Program, check this website: https://www.globalreporting.org/standards/sector-program/

The Ten Principles of United Nations Global Compact

The United Nations Global Compact defined in 2004 ten principles that provide companies strategies, policies and procedures to follow their sustainable responsibilities and setting the stage for long-term success. The areas of responsibility are human rights, labour, environment and anti-corruption.Human Rights

Principle 2: make sure that they are not complicit in human rights abuses.

Labour

Principle 4: the elimination of all forms of forced and compulsory labour;

Principle 5: the effective abolition of child labour; and

Principle 6: the elimination of discrimination in employment and occupation.

Environment

Principle 8: undertake initiatives to promote environmental responsibility; and

Principle 9: encourage the development and diffusion of environmentally friendly technologies.

Anti-Corruption

Sustainable Development Goals (SDG) (United Nations)

In 2015 the United Nations General Assembly defined the SDGs. It is planned to achieve all the 17 goals by 2030. They should demonstrate a “blueprint to achieve a better and more sustainable future for all.” Furthermore, the goals are defined to address the global challenges and are related to poverty, inequality, climate change, environmental degradation, peace and justice.

Read more about the individual goals: https://www.undp.org/sustainable-development-goals

After this overview of the evolution of sustainability, the following sections will introduce the different dimensions (social, ecological and economic) and show their influence on the movement of goods.

Sources

Bundesministerium für Arbeit und Soziales (2024): Corporate Sustainability Reporting Directive (CSRD). URL: https://www.csr-in-deutschland.de/DE/CSR-Allgemein/CSR-Politik/CSR-in-der-EU/Corporate-Sustainability-Reporting-Directive/corporate-sustainability-reporting-directive-art.html (last access 23.05.2024).

Elkington (1994): Towards the Sustainable Corporation: Win-Win-Win Business Strategies for Sustainable Development. California Management Review, 36, 90-100. http://dx.doi.org/10.2307/41165746

European Commission (2013): Green Paper - A 2030 framework for climate and energy policies. URL: https://eur-lex.europa.eu/LexUriServ/LexUriServ.do?uri=COM:2013:0169:FIN:en:PDF (last access 30.05.2024)

Global Sustainability Standards Board (GSSB) (2021): GRI Standards. URL: https://www.globalreporting.org/standards/ (last access 30.05.2024)

Institut für ökologische Wirtschaftsforschung und future e. V. – verantwortung unternehmen (Hrsg.) (2021): CSR Reporting in Deutschland 2021. URL: https://www.ioew.de/fileadmin/user_upload/BILDER_und_Downloaddateien/Header-Bilder/Publikationen/Ranking_Nachhaltigkeitsberichte_2021_Ergebnisbericht_1.pdf (last access 23.05.2024).

United Nations Global Compact (2020): The Ten Principles the UN Global Compact. URL: https://unglobalcompact.org/what-is-gc/mission/principles (last access 23.05.2024).

United Nations (1987): Brundtland Report. URL: https://www.are.admin.ch/are/en/home/media/publications/sustainable-development/brundtland-report.html (last access 27.05.2024).

United Nations (2015): Transforming our world: The 2030 Agenda for sustainable development. URL: https://sustainabledevelopment.un.org/content/documents/21252030%20Agenda%20for%20Sustainable%20Development%20web.pdf (last access: 30.05.2024)

United Nations (2023): Sustainable Development Goals, Guidelines for the use oft he SDG Logo. URL: https://www.un.org/sustainabledevelopment/wp-content/uploads/2023/09/E_SDG_Guidelines_Sep20238.pdf (last access: 30.05.2023)

Volker Hauff (Hrsg.) (1987): Unsere gemeinsame Zukunft. Der Brundtland-Bericht der Weltkommission für Umwelt und Entwicklung. Greven.

Wu (2013): The problems of weak sustainability and associated indicators. URL: https://www.researchgate.net/figure/From-Wu-2013-Illustration-of-the-triple-bottom-line-definition-of-sustainability-a_fig1_292346996 (last access 23.05.2024).

2. Social dimension

On the following page the social dimension of sustainability will be explained to you. After showing you the development of corporate social responsibility we are talking about the working conditions such as the dimensions and activities for companies.

Definitions of Corporate Social Responsibility (CSR)

According to Bowen (1953), the corporate social responsibility “refers to the obligation of businessmen to pursue those policies, to make those decisions, or to follow those lines of action which are desirable in terms of the objectives and values of our society.“

The European Commission (2001) states that Corporate social responsibility is basically a voluntary commitment by companies to work toward a better society and a cleaner environment.

CSR is closely linked to the already presented Ten principles of the United Nations Global Compact, which propose that companies should be required to make decisions not only on the basis of financial/economic factors, but also taking into account the social and environmental impact of their activities.

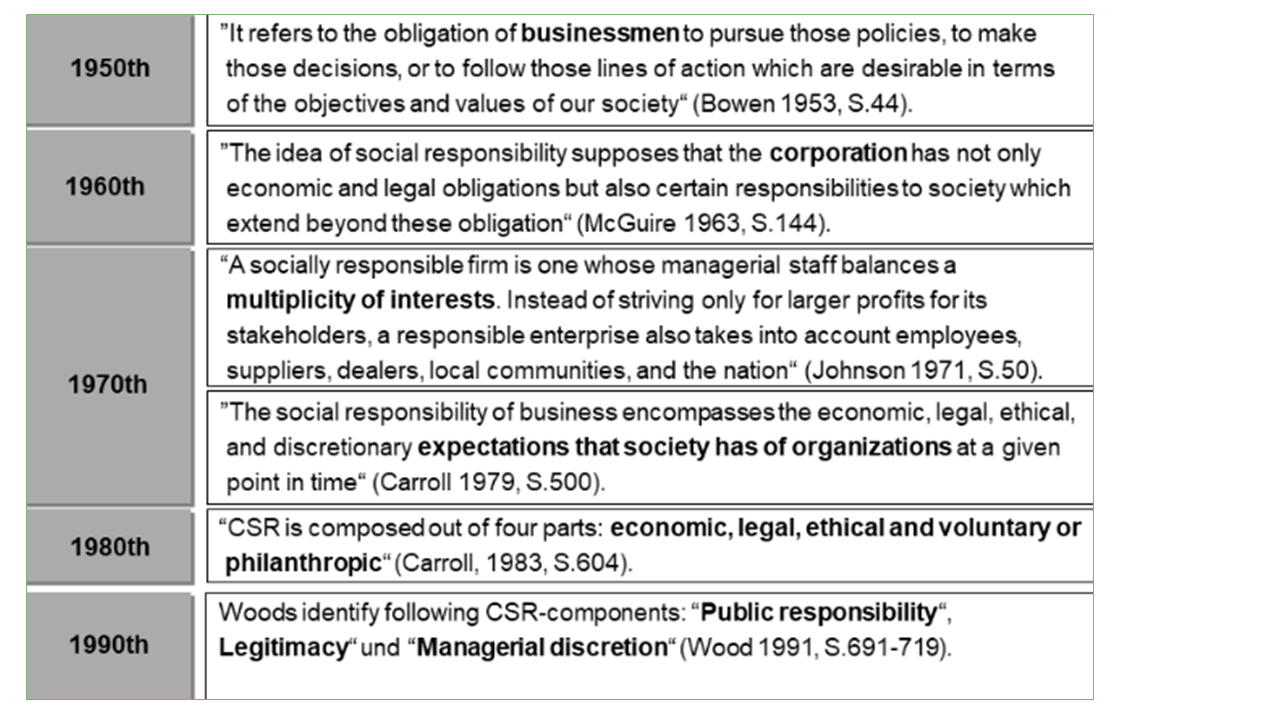

The following figure “Conceptual changes of Corporate Social Responsibility Concept over the years" shows the development of CSR from 1950 to 1990. Starting with a strong business and the obligation to follow the given policies, CSR has evolved and taken up more relevant criteria such as the expectations of the society, the multiplicity of interests, the public responsibility etc.

CSR for companies

CSR is a term used to describe what some consider to be a company's obligation to address the needs of all stakeholders in its business activities above and beyond legal requirements. The stakeholders of a company are all those who are influenced by, or can influence, a company’s decision and action. Stakeholders can be

- employees,

- customers,

- suppliers,

- community organizations,

- subsidiaries and affiliates,

- joint venture partners,

- local neighborhoods,

- investors, and shareholders (or a sole owner),

- financial and insurance institutions,

- and more...

Stakeholders are responsible for the value of companies. Over the last 20 years, their rates have become increasingly dependent on environmental and social standards, which are mostly formulated by environmental institutions.

Working conditions

Working conditions are an important pillar of the CSR standards, as companies could not operate successfully without their employees. For increasing the social sustainability of the companies, it is necessary to ensure better working conditions.

In the last years, the market conditions in logistics (Fast, Flexible, Cost-efficient and Heavy competitive pressure) lead to changing working conditions in industrialised countries:

- Long working times that are almost impossible to plan

- Outsourcing to third-party companies or bogus third-party companies

- Departure from normal working relationships

- Low pay

- Health and workplace conditions (heavy physical burden, working in noise and exhaust fumes, unhealthy way of life)

- Lack of balance between work and private life

- Job (dis)satisfaction

- Rising job requirements

Internal and external dimension of CSR in EU-green paper

In 2001, the European Commission defines the internal and external dimension of CSR for companies in their Green Paper: Promoting a European framework for Corporate Social Responsibility as follows:

Internal CSR dimension

- Human resource management

- Health and safety at work

- Adaptation to change

- Management of environmental impacts and natural resources

External CSR dimension

- Local communities

- Business partner, suppliers and consumers

- Human rights

- Global environmental concerns

Areas of impact of CSR

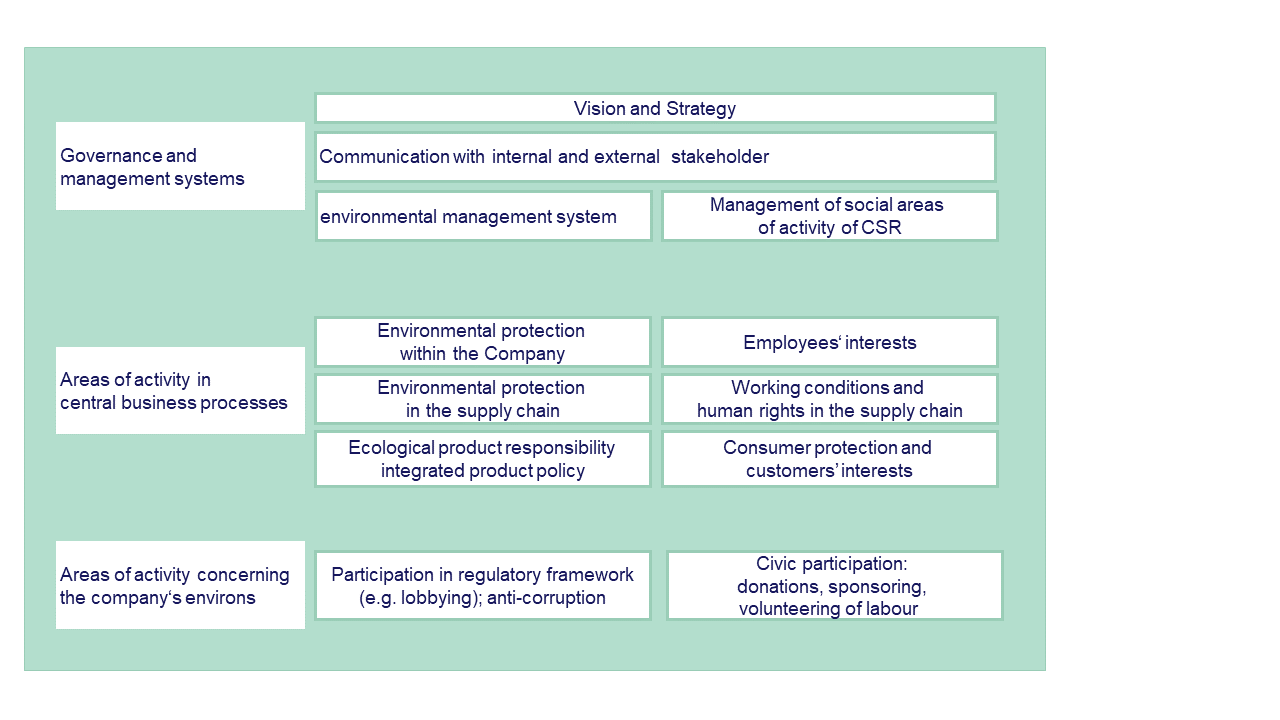

The following figure “Areas of impact of CSR” shows the influence of CSR on the company’s organization chart. CSR affects all areas of a company and covers all activities in the governance and management systems, all areas of activity in central business processes and all areas of activity concerning the company’s environment. A more sustainable vision and strategy impacts the whole company, while the communication with internal and external stakeholders, the environmental management system and the management of social areas of activity of CSR are changing the governance and management systems of a company. The environmental protection, improved working conditions or an ecological product responsibility are impacting the central business processes. The company's environment is changed by the participation in regulatory framework and the civic participation.

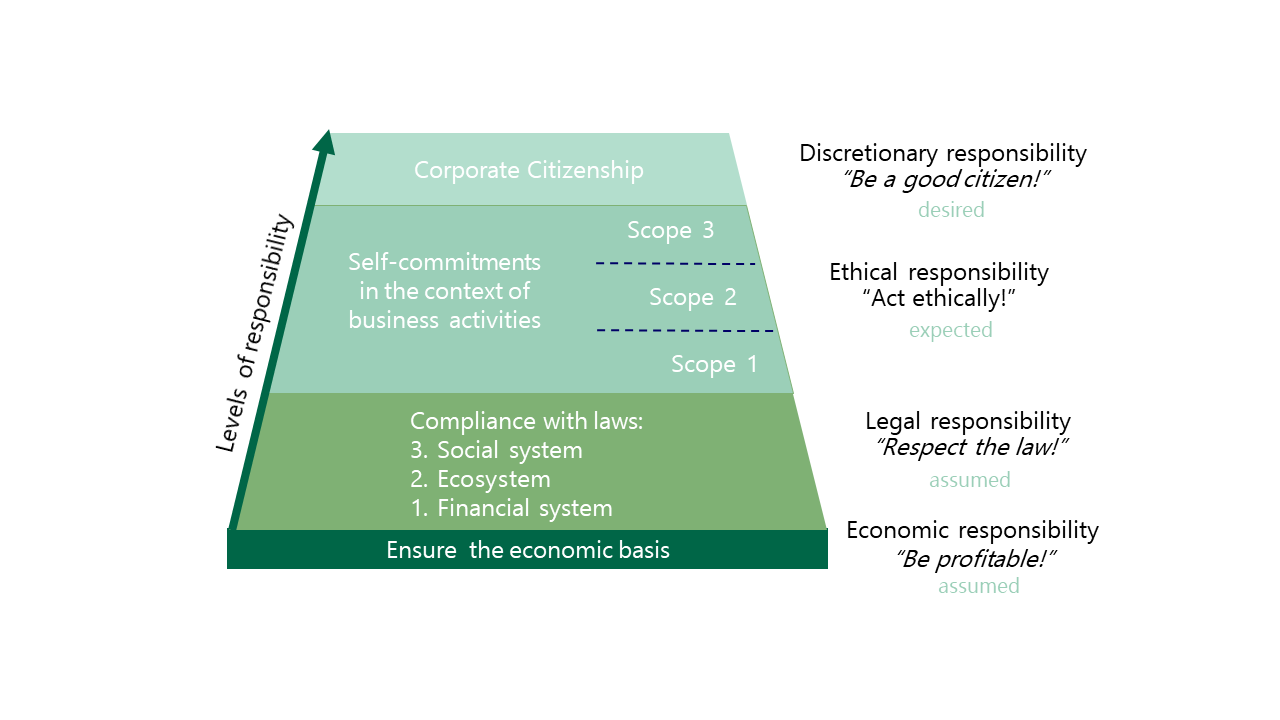

From compulsory to voluntary exercise: Levels of Corporate Social Responsibility

The following figure “Levels of Corporate Social Responsibility” shows the different levels of CSR, that can be reached. While the lower levels are compulsory, the upper levels are voluntary. The base is to ensure the profitability and to act responsible in terms of the well-being of the company. The next level is to ensure compliance with the law (legal responsibility). After those two compulsory levels, the next step to higher the level of CSR, the companies need to act ethically, which means that they can self-commit their business activities in terms of the three scopes which will be explained on the next page. The highest level of CSR is reached when there is really a corporate citizenship, which means that the company is acting like a good citizen.

Competition

Sustainability reporting and labelling are becoming increasingly important in a competitive environment. Today, the topics that companies deal with are defined in a multi-stakeholder process. An in-depth look at the activities of companies shows the concentration of measures on win-win measures, i.e. economic-ecological efficiency.On the next page, you will find out more about the ecological dimension of the movement of goods.

Sources

Bowen, H. R. (1953): Social Responsibilities of the Businessman. New York, Harper and Brothers. Commission of the European Communities (Ed.) (2001).

Bundesministerium für Umwelt, Naturschutz und Reaktorsicherheit (BMU) (Ed.) (2006): Corporate social Responsibility Eine Orientierung aus Umweltsicht.

Carroll, A. B. (1979): "A Three-Dimensional Conceptual Model of Corporate Performance." Academy of Management Review 4(4): 497-505.

Carroll, A. B. (1983): "Corporate Social Responsibility: Will industry respond to cutbacks in social program funding?" Vital Speeches of the day 49: 604-608.

Carroll, A. & Buchholtz, A. (2003): Business & Society. Ethicx and Stakeholder Management. Ohio.

Drewes, P. (2012): Corporate Sustainability Management (CSM) in der Containerschifffahr. Harburger Berichte zur Verkehrsplanung und Logistik, Band 10, Schriftenreihe des Instituts für Verkehrsplanung und Logistik. Technische Universität Hamburg-Harburg. ISBN 978-3-86991-702-3

McGuire, J. W. (1963): Business & Society New York, McGraw-Hill

Wood, D. J. (1991): "Corporate Social Performance Revisited." Veröffentlichungsreihe der Abteilung Organisation und Technikgenesung des Forschungsschwerpunkts Technik Arbeit-Umwelt des Wissenschaftszentrums Berlin für Sozialforschung(FS II 91-101): 0-34.

3. Ecological dimension

On the following page the ecological dimension of sustainability will be explained to you. After showing you the consequences of climate change and GHG emissions on the world we are talking about the reporting standards for companies and explain you, how to calculate emissions from goods movement.

Transport and environment

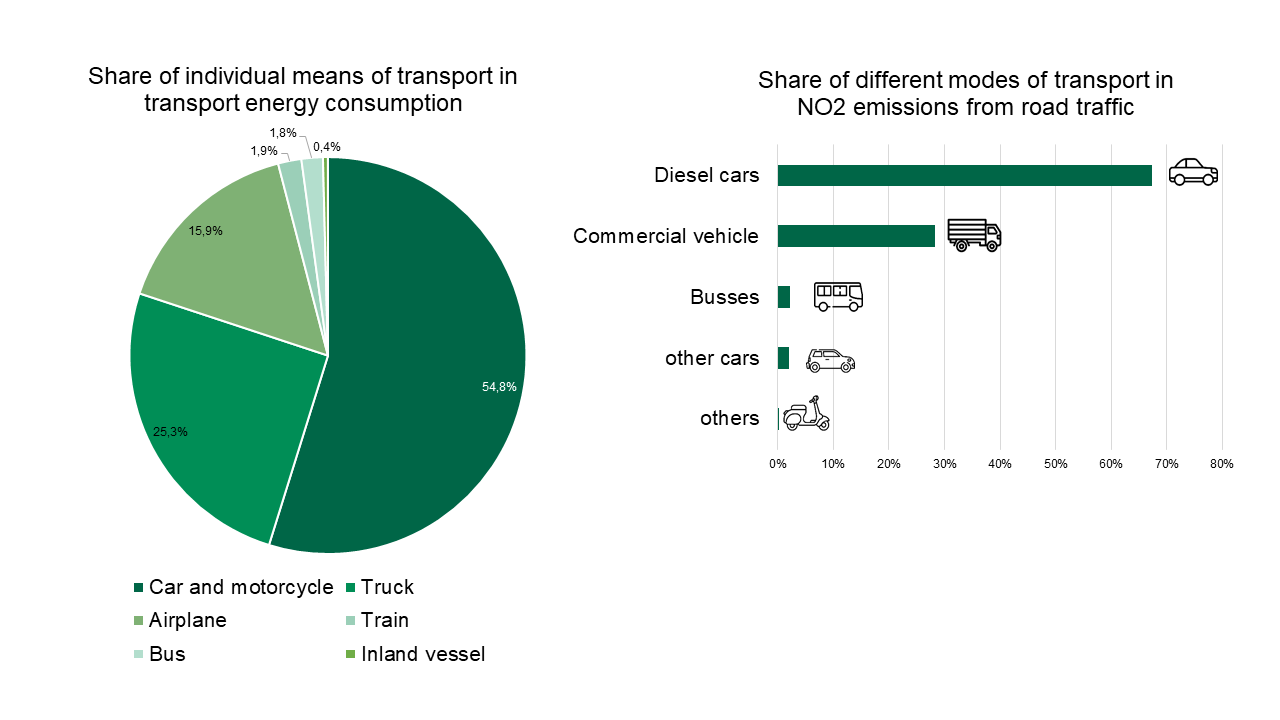

The following figure „Share of different modes of transport in energy consumption and NO2 emissions” shows the different movables and their transport energy consumption in 2022 such as their Nitrogen dioxide (NO2) emissions in 2021 from road traffic. NO2 is a corrosive irritant that is released during combustion processes in systems and engines. It contributes to particulate matter pollution and can increase the risk of dying from cardiovascular diseases and also contributes to the over-fertilisation and acidification of soils.

In Germany, 2.5 acres of new land was taken up for transportation purposes each day in 2019. Every year, 111,420 tons of plastic microparticles are released by tire abrasion into the environment in Germany alone. In 2017, 13.2% of the population in Germany was affected by sound levels above 50 decibel (dB(A)). 50 dB(A)corresponds to a normal room volume and is just about comfortable for us. Outside the home, average noise levels above 55 dB(A) are likely to have an increasingly negative impact on our mental and social well-being.

Why is the focus on carbon dioxide (CO2) or equivalent balances?

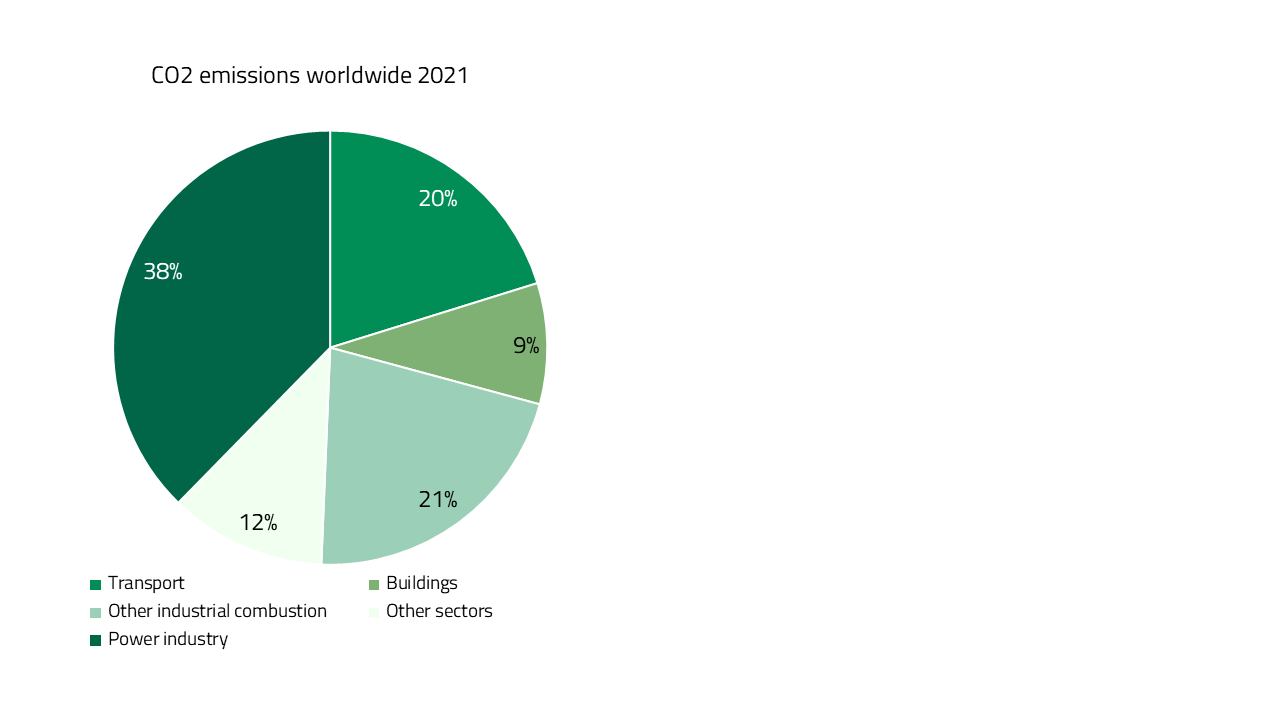

The following figure “CO2 emissions worldwide 2021” shows the emissions in the sectors transport, buildings, other industrial combustion, power industry and other sector.

There is a linear dependence of CO2 on energy use (regardless of the kind of fuel). The anthropogenic CO2 is the GHG number 1. Greenhouse gases are a group of gases contributing to climate change and global warming and are explained to you below. Worldwide, 20 % of global CO2 emissions are caused by transport (passengers and goods). There exist policy steering parameter like the Kyoto Protocol. In a non-binding communiqué issued on June 7 2007, it was announced that the G8 nations would ‘aim to at least halve global CO2 emissions by 2050’.

The logistics sector is highly dependent on fossil fuels and has a high growth rate. In total, Logistics accounts for 10-11% of global CO2 emissions, where

- the Transport of goods accounts for approx. 8%

- the Storage and terminals accounts for approx. 1-2%

- while the accounts for Administration and IT are unknown.

Use of resources

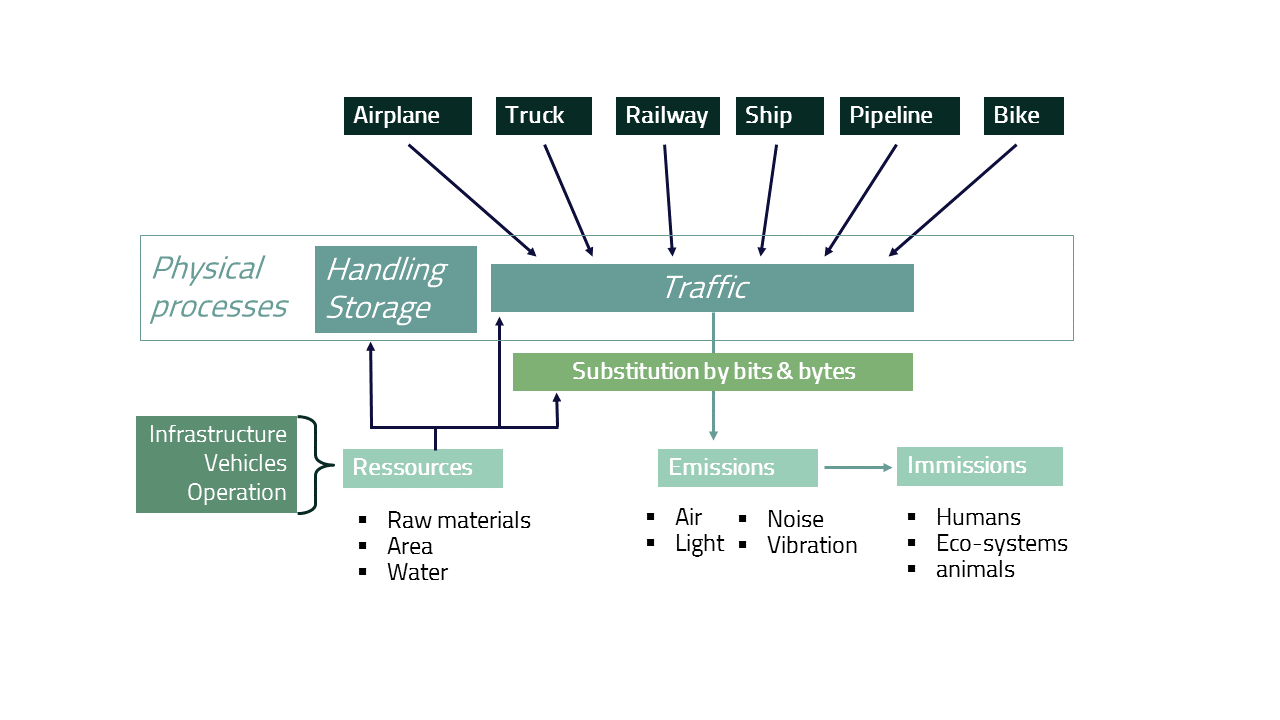

The following figure "Relationship between transport, resource consumption and environmental use" shows, how the use of resources like raw materials, area, water but also infrastructure, vehicles and operation leads to emissions and immissions. The resources are needed for handling, storage and traffic. Sometimes, a substitution of traffic through bits and bytes is possible, but this also leads to resource consumption and emissions from different resources and emissions elsewhere (spatial shift of the problem).

Traffic can be generated by different movables (e.g. airplane, truck, train) and leads to emissions like air, noise, light or vibration. Those emissions themselves are leading to immissions for human beings or animals.

Consequences of climate change

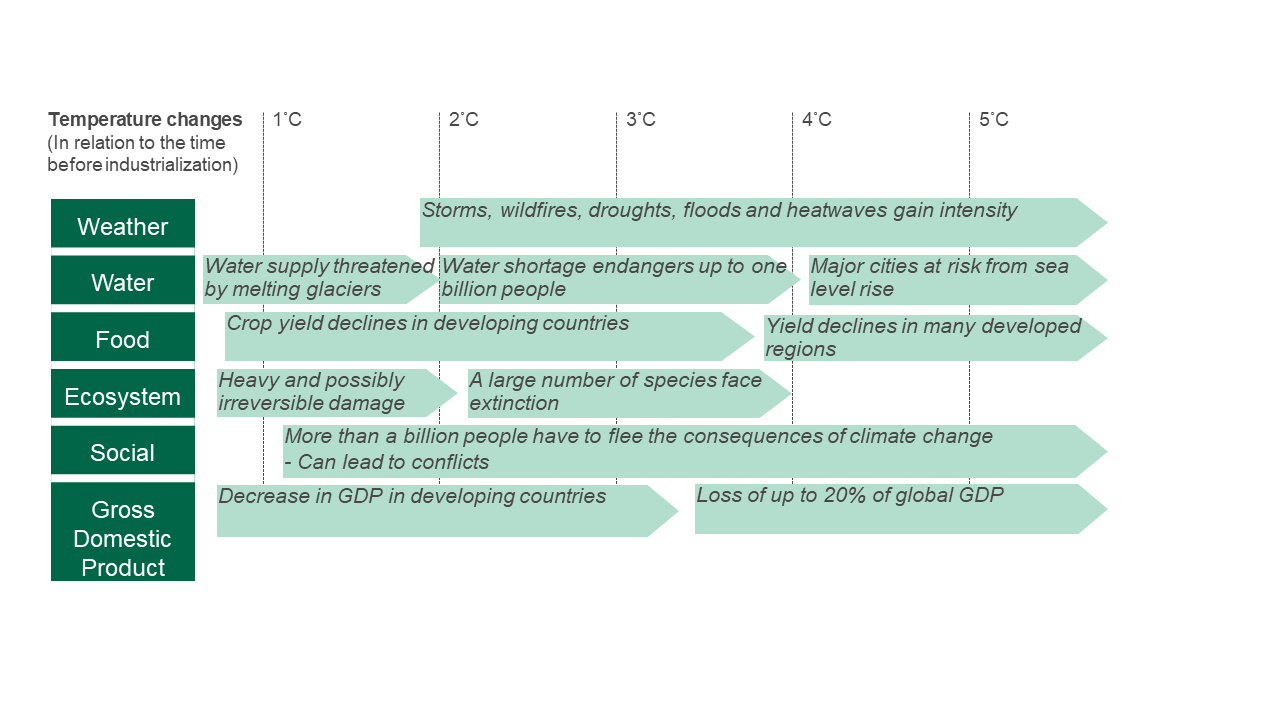

The consumption of resources and the resulting emissions and immissions lead to an increase in temperature. This ongoing temperature changes have an impact on several aspects e.g. weather, water, food and the ecosystem. The following figure “Consequences of climate change” shows, how different temperature changes are impacting the weather, water, food, ecosystem, social and the gross domestic products. An increase of just 1 degree will threaten water supplies through melting glaciers and results in a crop yield decline in developing countries, a severe and irreversible damage to ecosystems, a first refugee movements (‘climate refugees’) and a reduction in GDP in developing countries. From a 2 degree increase, there will also be an increase in extreme weather events, a water shortage for up to one billion people and the extinction of many animal species. At the UN Climate Change Conference (COP21) in Paris 12 December 2015, 196 parties adopted a legally binding international treaty on climate change. The goal is to hold “the increase in the global average temperature to well below 2°C above pre-industrial levels” and pursue efforts “to limit the temperature increase to 1.5°C above pre-industrial levels.” (United Nations 2015)

Definitions of Greenhouse gas

When talking about emissions, climate change and global warming, the three terms GHG, GWP and CO2e are often used, which are defined according to the ISO 14083 as follows:

Greenhouse gas (GHG): Gaseous constituent of the atmosphere, both natural and anthropogenic, that absorbs and emits radiation at specific wavelengths within the spectrum of infrared radiation emitted by the Earth's surface, the atmosphere and clouds.

Global warming potential (GWP): Index, based on radiative properties of GHG, measuring the radiative forcing following a pulse emission of a unit mass of a given GHG in the present-day atmosphere integrated over a chosen time horizon, relative to that of carbon dioxide (CO2).

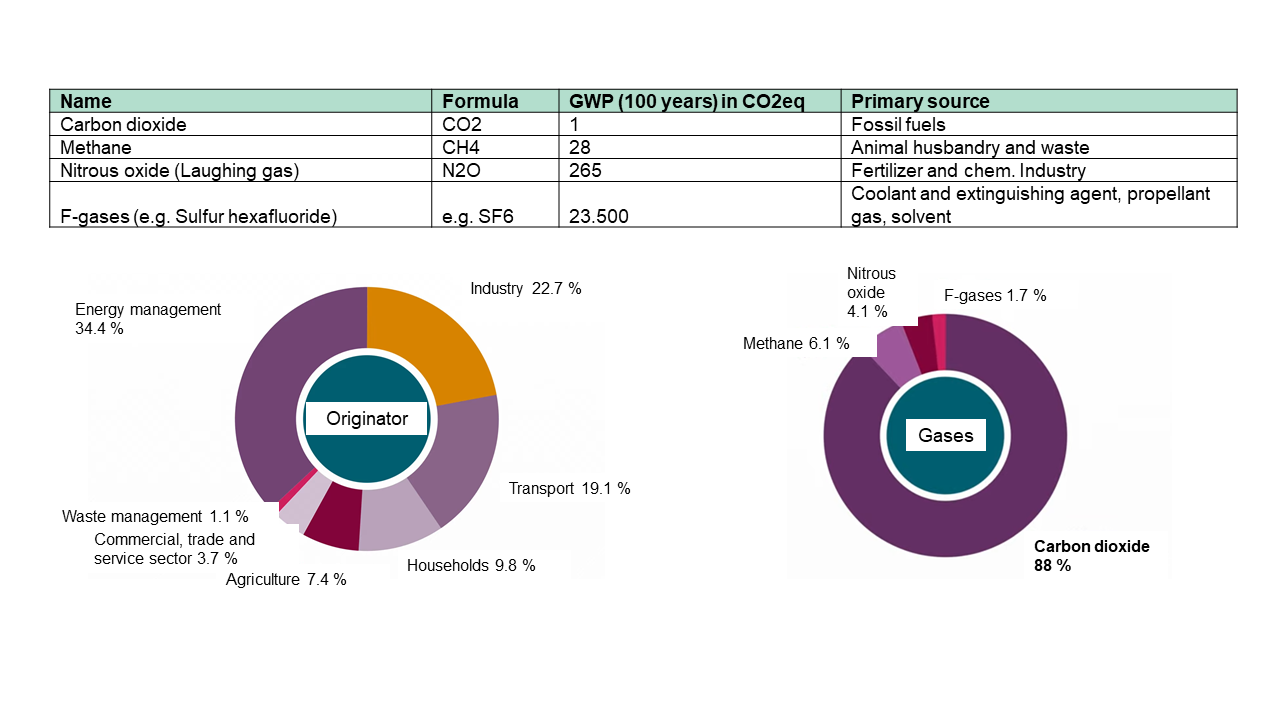

Carbon dioxide equivalent (CO2e): Unit for comparing the radiative forcing of a GHG to that of carbon dioxide. The carbon dioxide equivalent is calculated using the mass of a given GHG multiplied by its global warming potential.The following figure “Greenhouse Gases - Originator, Gases and GWP” shows you the different greenhouse gases like carbon dioxide, methane, nitrous oxide and f-gases, its formula, GWP (in 100 years) in CO2eq and primary source. Furthermore, the graphs provide information about the originators of the gases and the distribution of the gases. 19,1 % of the GHG emissions originate from transport. From the GHG, 88% are CO2, 6,1 % Methane, 4,1 Nitrous oxide and 1,7 % F-gases.

Legislation

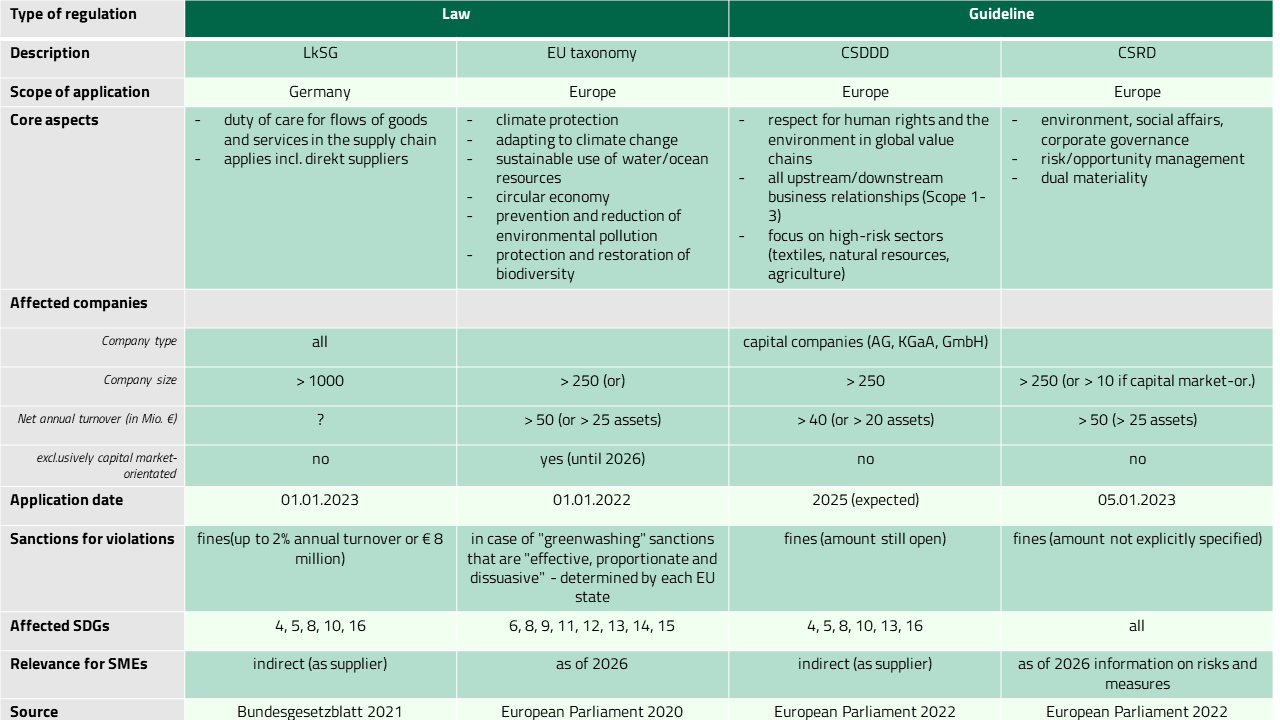

As already mentioned on the previous pages, the EU has issued important legislations for the past and coming years to ensure a standard for sustainable behaviour. The following figure “Legislations: Affected companies and relevance for SMEs” (small and medium-sized enterprises) shows you four important legislations (Regulations and Directives) for Germany and Europe and the companies affected. While the LkSG (Lieferkettensorgfaltspflichtengesetz) is a German regulation, the EU taxonomy as well as the CSRD (Corporate Sustainability Reporting Directive) and the CSDDD (Corporate Sustainability Due Diligence Directive) are EU directives that are defining goals, EU countries must achieve.

The four legislations are explained in detail below.

LkSG

EU taxonomy

The EU taxonomy regulation (EU) 2020/852 is a classification tool for corporate activities and their contribution to sustainability and a reference point for investors to assess the sustainability of companies. It is a mandatory reporting since 2022 and is established for benchmarks and values. The objectives are more investments in sustainable technologies and companies and to encourage companies to act "greener”. The scope of application is large capital market-oriented companies with more than 250 employees that are not financial companies and have a net sales of 50 million € or a balance sheet of more than 25 million €. Furthermore, it also applies to listed SMEs and other companies. The EU taxonomy should provide criticism of the classification of individual activities (e.g. gas and nuclear energy).

The EU taxonomy has the following six environmental goals:

- Prevention of climate change

- Adaptation to climate change

- Sustainable use and protection of water and marine resources

- Transition to a circular economy

- Pollution prevention and control

- Protection and restoration of biodiversity and ecosystems

The EU taxonomy was amended on 4 June 2021 as part of a delegated regulation. It stipulates that the following substantial contribution to climate change adaptation must be done by the freight transport services by road:

- The vehicles should not be intended for fossil fuel transportation

- The vehicles (N1, N2, N3) must be reusable or recyclable to a minimum of 85 % by weight

- From 1 January 2026, vehicles in category N1 may no longer cause direct CO2 exhaust emissions

- Vehicles in categories N2 and N3 with a technically permissible maximum mass of 7.5 tonnes or less must be ‘zero-emission heavy-duty vehicles’* or, if this is not technically and economically feasible, ‘low-emission heavy-duty vehicles’*

A critical aspect of the taxonomy is that only direct emissions are assessed and that transport companies have to retrofit their vehicle fleets.

The current status of the EU taxonomy can be found here and the EU taxonomy here.

CSDDD

The CSDDD obliges large European and foreign companies throughout the EU to comply with certain environmental and human rights standards in their supply and value chains. It is built on the LkSG, but extends the environmental due diligence obligations and also includes chemical-related obligations and obligations to protect biodiversity, endangered species and specially protected areas and seas. In addition, companies must draw up and implement a plan to minimise their impact on climate change. To this end, companies must ensure that their business model and strategy are compatible with limiting global warming to 1.5 degrees and the transition to a sustainable economy.

You can find more information on the CSDDD here and the directive here.

CSRD

The "Corporate Sustainability Reporting Directive - CSRD," Directive (EU) 2022/2464 entered into force on 5 January 2023. With this directive large and listed companies are required to publish regular annual reports on their social and environmental risks and explain how their activities affect people and the environment.

The first companies will have to apply the new rules for the first time in the 2024 financial year, for reports published in 2025. With the CSRD, the number of companies in the EU that must publish reports will significantly increase from 11,600 to up to 49,000. (~15.000 in Germany). From the 2026 financial year, listed small and medium-sized enterprises (more than 10 employees and/or more than 450.000 € total assets and/or more than 900.000 € net annual turnover), small and non-complex credit institutions and captive insurance companies must also prepare a CSRD report. Micro-enterprises are exempt from this directive.

The CSRD includes the following innovations:

- Expanded and standardized reporting requirements: Companies are encouraged to adapt their reports and adhere to uniform rules. This enhances measurability and comparability through figures and data. The rules are developed by the European Financial Reporting Advisory Group (EFRAG).

- Redefinition of materiality: The requirements for sustainability reporting introduce the concept of double materiality. Companies must now report how their activities affect society and the environment and how important sustainability is for themselves. Previously, they only had to report if both aspects were significant.

- Mandatory external audit: Similar to financial reports, sustainability reports must now also be audited by a third party according to specific standards. The exact auditing rules are determined by the EU Commission. Initially, an audit providing "limited assurance" is required, but this will later be expanded to "reasonable assurance," similar to the auditing of financial reports.

- Integration into the management report: To ensure sustainability information is easily accessible, it must now be included in the management report. This highlights the increasing importance of sustainability reports, similar to financial reports.

You can find more information about the current status of the CSRD here and the CSRD here.

There are also more product-related sustainability policies and regulations, that are listed below:

- REACH Directive (1907/2006/EC)

- WEEE Directive (2002/96/EC)

- Buildings Directive (2002/91/EC)

- RoHS Directive (2002/95/EC)

- European Energy Star (2422/2001/EC)

- Landfill Directive (99/31/EC)

- Packaging Directive (94/62/EC)

- Batteries Directive (91/157/EEC)

- Fluorescent Lighting (2000/55/EC)

- Domestic Refrigeration (96/57/EC)

- Hot-Water Boilers (92/42/EEC)

- Energy Labelling (92/75/EEC)

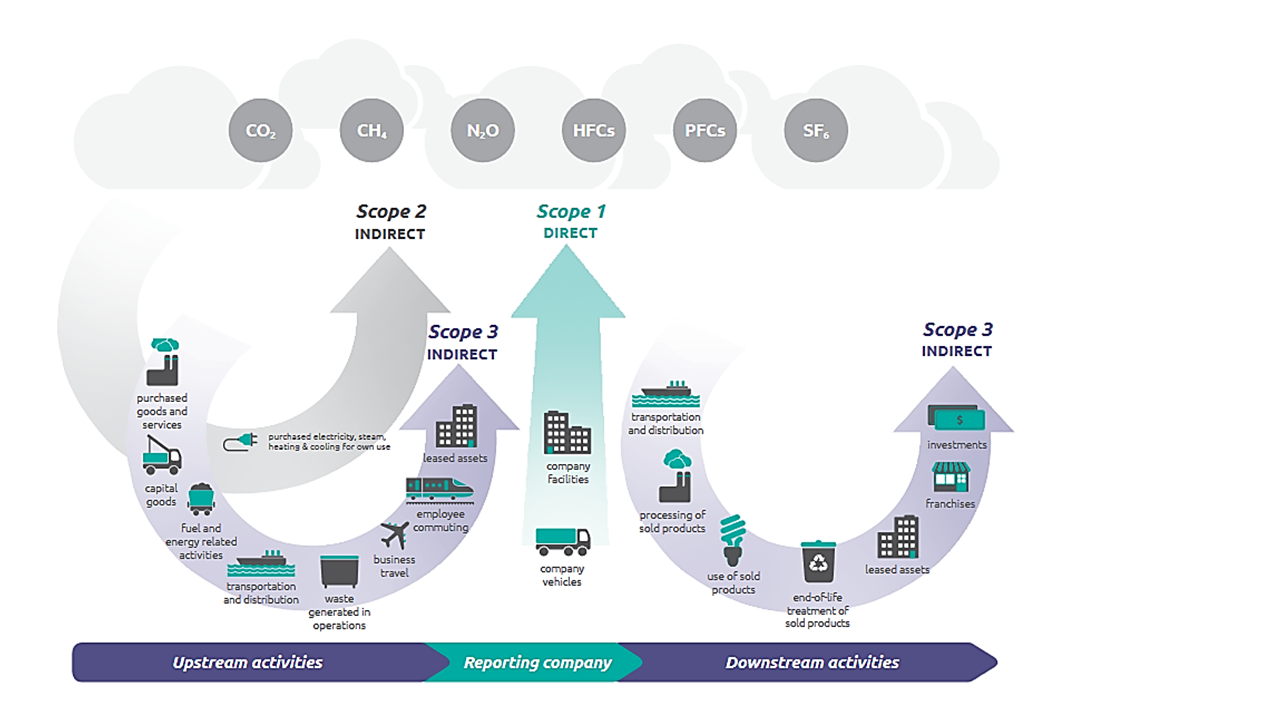

GHG Protocol scopes and emissions across the value chain

The Greenhouse Gas Protocol with World Business Council for Sustainable Development and World Resources Institute (WRI) are the main drivers to develop calculation and evaluation standards for companies. The first standards for products and supply chain GHG (scope 3) were developed at the end of 2011.

The following figure “Illustration of the Greenhouse Gas Protocol” shows the Scopes 1, 2 and 3 of emissions and the indirect and direct effects (CO2 (carbon dioxide), CH4 (methane), N2O (nitrous oxide), HFCs (hydrofluorocarbon), PFCs (perfluorcarbon) and SF6 (sulfur hexafluoride)). Scope 1 emissions cover emissions controlled or owned by a company e.g. burning fuel in the fleet of company vehicles. Scope 2 emissions are indirectly generated emissions resulting from the use of purchased electricity, steam, heat or cooling. Scope 3 emissions include all other indirect emissions caused by a company's activities in its value chain that are not produced by a company itself. This includes in the upstream activities e.g. upstream transport and distribution, waste generated in operations, business travel or other purchased goods and services. The downstream activities for scope 3 emissions include the downstream transport and distribution, the processing and utilisation of products sold, the end-of-life treatment of products sold or franchises and other investments.

According to the GHG Protocol (2004) and the International Organization for Standardization (ISO) 14083, the General GHG Accounting and Reporting principles for companies are as follows:

- Relevance: GHG sources, GHG sinks, GHG reservoirs, data and methods are selected according to the needs of the intended user.

- Completeness: All relevant GHG emissions and removals are included.

- Consistency: Meaningful comparisons of GHG-related data are made possible.

- Transparency: Sufficient and appropriate GHG-related information is disclosed to enable intended users to make decisions with reasonable confidence.

- Accuracy: Deviations and uncertainties are reduced as far as possible.

- Conservativeness: When evaluating comparable alternatives, a selection is made that is cautiously moderate.

Standards

- ISO 14001: environmental management systems

- ISO 14040/14044: life cycle assessment (LCA)

- ISO 14064: Tools for evaluation, verification and reporting of GHG emission

- ISO 14067: Carbon Footprints of Products

- ISO 14083: Greenhouse gases — Quantification and reporting of greenhouse gas emissions arising from transport chain operations

ISO 14083 – Quantification and reporting of greenhouse gas emissions arising from transport chain operations

ISO 14083 is a set of guidelines for the calculation and reporting of greenhouse gas emissions caused by the transportation of people and goods. As such, it is primarily used by companies or individuals operating in the logistics sector. The standard was published in March 2023 and replaces the EN 16258:2021 "Methodology for calculation and declaration of energy consumption and GHG emissions of transport services (freight and passengers)". In addition to the transport operations contained in the old standard, the new ISO 14083 also includes processes and the associated GHG emissions at locations (hubs) that enable the transfer of passengers or freight

The standard includes the following aspects:- Requirements and guidance for the quantification, assignment, allocation and reporting of greenhouse gas (GHG) emissions for transport chains for passengers and freight.

- Claim of universal use (e.g. both multinational organizations with multimodal transports and small regional carriers).

- GHG emissions from vehicle and hub operations (Scope 1).

- Explicit integration of associated energy provision (Scope 2).

- The standard includes freight and passenger transportation

- Focus on Scope 1 and 2 of transportation operations.

The ISO 14083 contributes to the carbon footprint of products (ISO 14067) and companies (ISO 14064) as well as to the life cycle assessment (ISO 14040 and ISO 14044). An isolated application of the standards is not intended. It illustrates interaction with other ISO standards in the ISO 14040 and ISO 14060 series and uses a product purchased online as an example. The GHG emissions intensity per tonne-kilometer (tkm) calculated according to ISO 14083 can be used as primary or secondary data for GHG quantification projects and the data would need to be adjusted or modified for this purpose to reflect GHG emissions on a whole life basis.

For the GHG inventory of a company, the ISO 14064-1 can be used. One component here is emissions from transportation. For calculating the emissions from transportations, the different steps of the product need to be taken into account. For calculating the carbon footprint of a product, the ISO 14067 can be used. In order to calculate the GHG emissions from the transport chain, the ISO 14083 is used. The Principles and framework for LCA in ISO 14040/44 are taken into account the ISO 14083 and ISO 14067. The results from the ISO 14067 and ISO 14083 are included in the GHG inventory and report, transport chain GHG report and Carbon Footprint of Products (CFP) study, which are used for the GHG statement. The GHG statements can be verified and validated by using the ISO 14064-3, which builds upon the ISO 14065 (General principles and requirements for bodies validating and verifying environmental information).

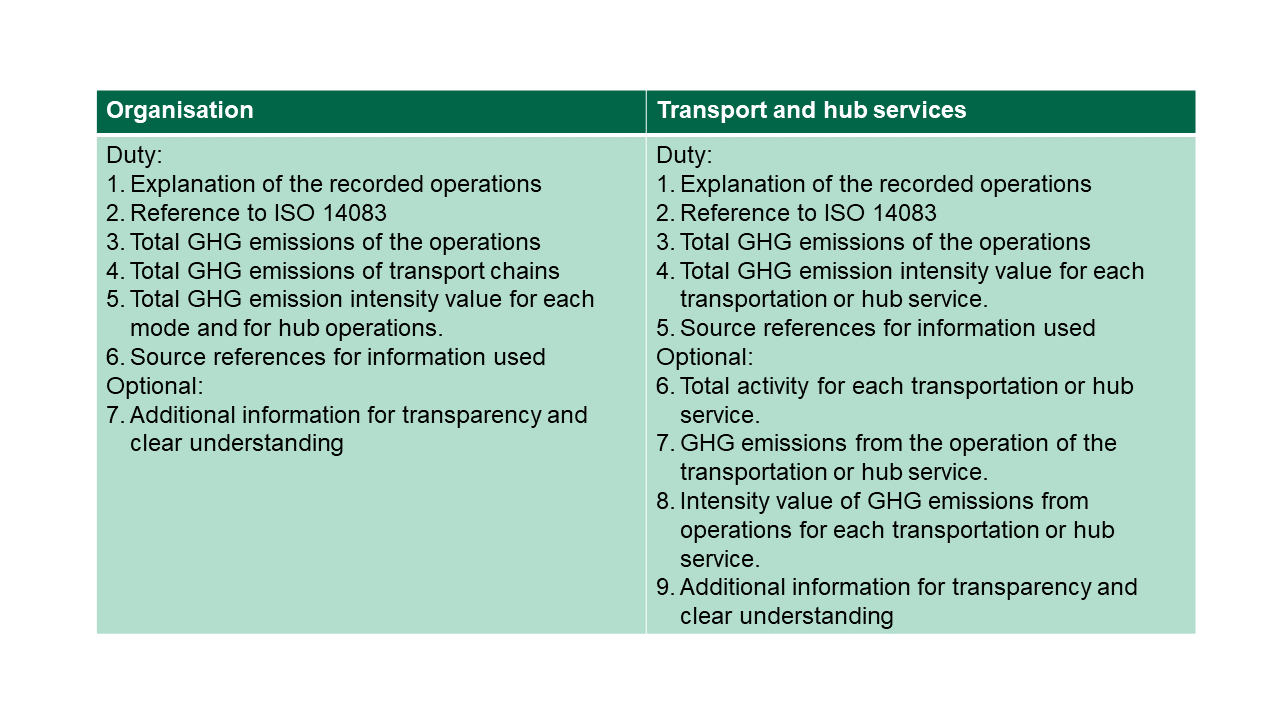

According to ISO 14083, reporting must take place at least once a year. The levels of reporting contain the overall organisation (e.g. company or group) such as the transport and hub services. The following figure “Reporting contents in accordance with ISO 14083 for organisations/transport and hub services" shows you the duties and optional reporting contents of the organisation and the transport and hub services in detail.

Transport chain-related GHG emissions considered in ISO 14083

Greenhouse gas emissions from the following categories are taken into account in ISO 14083:

- vehicle operation

- lifting process

- energy supply for the vehicle

- energy supply for the hub

- packaging life cycle (GHG packaging life cycle)

- grams (g),

- kilograms (kg)

- or tons (t)

In order to quantify the GHG emissions of the transport chain, the transport chain must be divided into successive Transport Chain Elements (TCE). The TCEs reflect the associated vehicle types, tube capacities and hubs that transport, handle or transfer freight and/or passengers as part of the overall transport chain. As an example, the transport chain can be divided into five TCEs, which are required for the greenhouse gas calculation. The TCE 1 and TCE 5 are representing road services, while the TCE 2, 3 and 4 are part of the shipping services. TCE 3 stands for the transport by ship, while TCE 2 and 4 include transshipment activities. The transport chain starts from the Freight consignor and ends at the Freight consignee.

TCEs can represent the following elements of the transport chain:

- Transport:

- All modes of transportation (road, rail, inland waterways, sea, air, and pipelines)

- All means of transport (e.g. ship, vehicle, aircraft)

- Transshipment between two TCE

- Hubs and terminals

- Empty runs due to subsequent transport

In order to quantify the GHG emissions, information needs to be exchanged between the participants in the transport chain.

Approach for the quantification of GHG emissions

If you want to quantify the GHG emissions, you can follow this five steps approach.

Step 1: Definition of system boundaries (SB)

Step 2: Determination of consumption and transport data

Step 3: Determination of emission factors

Step 4: Calculation of GHG emissions

Step 5: Documentation of results

Step 1: Definition of the system boundaries

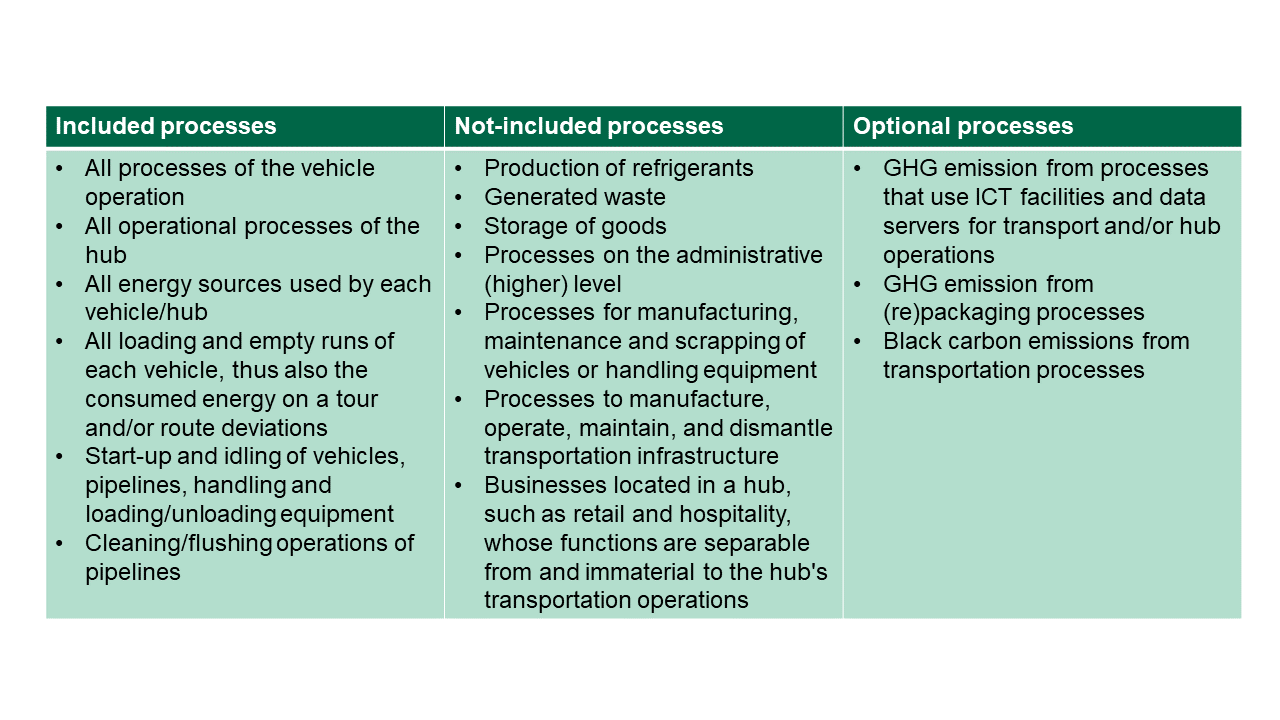

The figure "Definition of system boundaries of GHG emission quantification" supports you in defining the system boundaries. It shows, which processes are included, e.g. all processes of the vehicle operation, all operational processes of the hub and all energy sources used. For this, you need to consider the entire life cycle of the energy sources used (combustion and/or loss processes at the level of the vehicle or lifting equipment and all processes for providing energy). Processes like the production of refrigerants, the generated waste or the storage of goods are not included. GHG emissions from processes, that use ICT facilities and from (re)packaging as well as black carbon emissions (black material emitted from coal-fired power plants, gas and diesel engines and other sources that burn fossil fuel, which comprises particulate matters (PM) also) from transportation processes can be included.

- SB1: TTW (tank to wheel): direct vehicle emissions

- SB2: WTW (well to wheel): including energy supply chain

- SB3: includes maintenance and service of vehicles and infrastructure

- SB4: includes production and scrapping of freight vehicles

- SB5: includes administration, IT and personnel

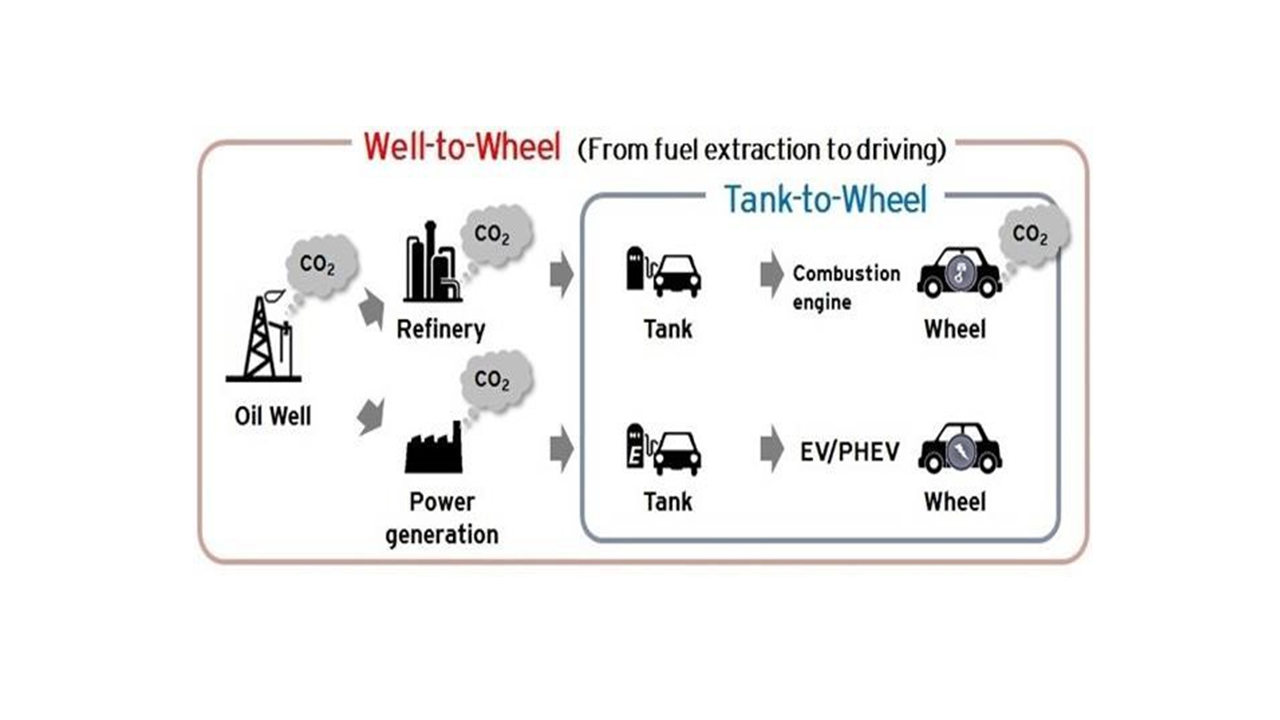

The following figure "Included processes for WTW and TTW” illustrates the different system boundaries of Well-to-Wheel and Tank-to-Wheel. With the Well-to-Wheel approach the entire chain from the fuel extraction to driving is being investigated taking into account the oil well, the refinery and the power generation but also the TTW emissions. Tank-to-Wheel focuses at the chain of effects from the energy absorbed to the conversion into kinetic energy in motor vehicles. The last measuring device before the final energy is transferred to the vehicle is usually installed in the filling station/charging station.

Step 2: Determination of consumption and transport data

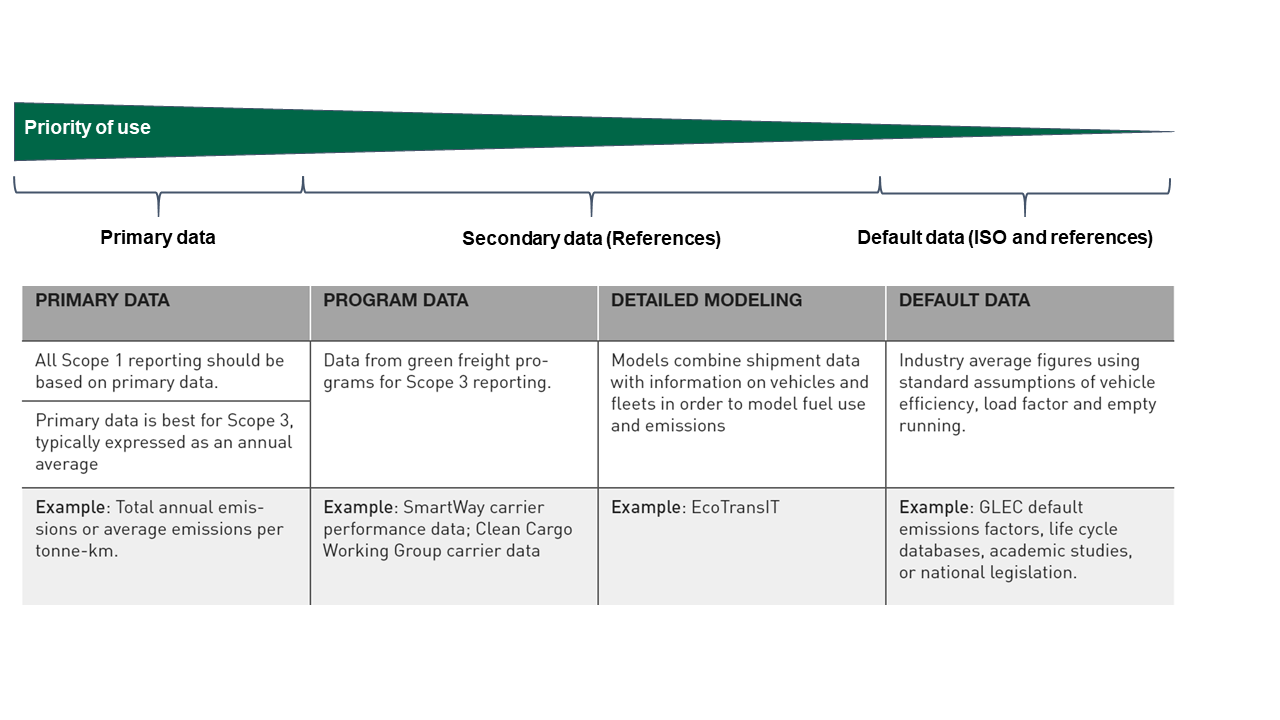

When determining the consumption and transport data, different data categories can be used. The following figure “Different data categories” shows you the categories primary data, secondary data (program data and detailed modelling) and default data and their priority of use. Ideally, primary data is used to calculate GHG emissions, especially for scope 1 reporting of own emissions. Ideally, scope 3 emissions are also calculated using primary data. However, as this is not always available, secondary data (e.g. from green freight programmes for scope 3 reporting or from detailed models) can also be used. Only if neither primary nor secondary data is available, default data (e.g. from ISO standards) should be used.

Step 3: Determination of emission factors

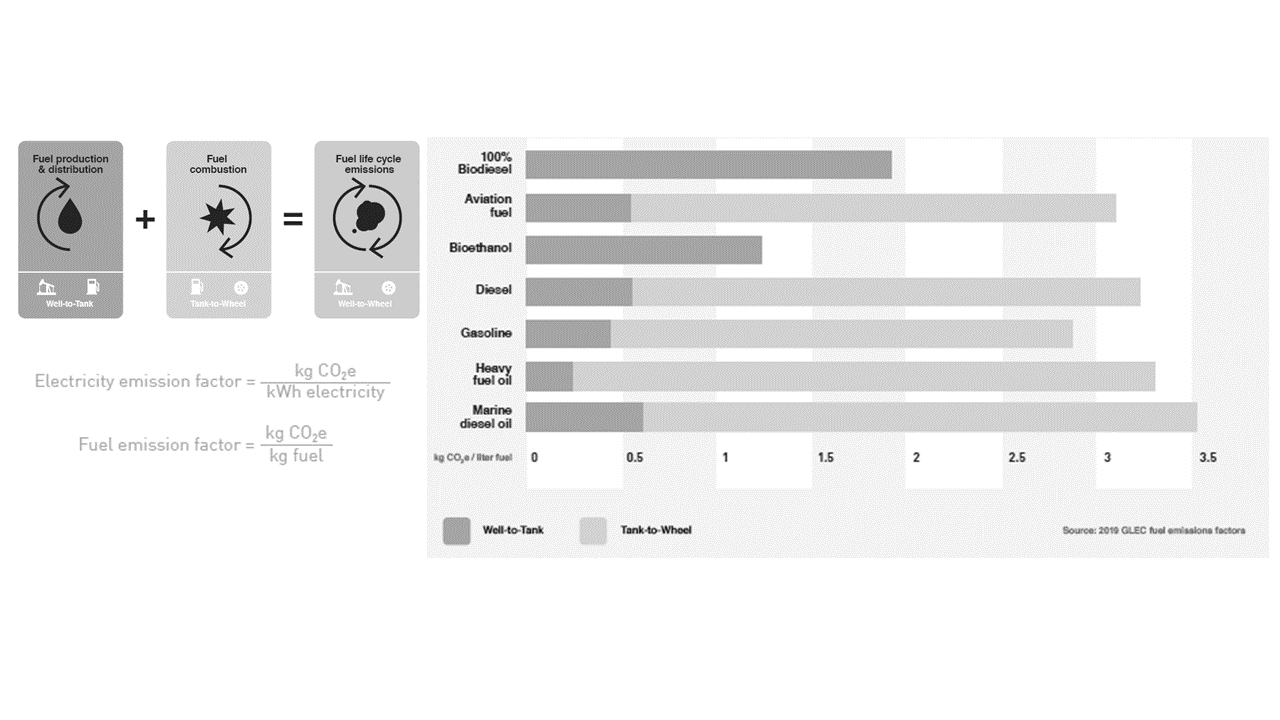

The following figure “Shares of WTT and TTW in WTW” shows the shares of well to tank (WTT) from fuel production and distribution and TTW from fuel combustion in the WTW (fuel life cycle emissions). It can be stated that the calculated emissions when burning 100% biodiesel are only from the fuel production and distribution (WTT). When using diesel, only around 16 % of the emissions are generated during production and distribution, while around 84 % are generated during fuel combustion. The figure shows why it is important to consider not only the TTW but also the WTT emissions, as this is the only way to map the entire fuel life cycle emissions.

The emission factors or GHG intensity values are calculated for both electricity and fuel by dividing the kg CO2e by the kWh of electricity or kg of fuel and are given in g CO2e/MJ or kg CO2e/kg. In the case of freight transport, the CO2e per tonne-kilometer or equivalent units and for freight throughput at the hub the CO2e per metric ton are used. Furthermore, the following denominators are commonly used in the logistics industry:

- Ton kilometres (tkm) or vehicle kilometres (vkm)

- Pallets or boxes delivered

- TEU or TEU-km

The figure "Calculation of emission factors/intensity value" shows the calculation of the GHG intensity value per pallet delivered. In this example, the delivery of all pallets (200 pieces) leads to 700 kgCO2e. So per pallet, 3.5 kgCO2e are emitted.

Step 4: Calculation of GHG emissions

Once the system boundaries have been defined and the consumption and transport data as well as the emission factors have been determined, the greenhouse gas emissions can be calculated. For this purpose, carbon calculators can be used.

You can find many carbon calculators online. They are developed by national or local governments, NGOs or consulting firms.

- A few examples:

- CarbonCare Asia Ltd.: https://www.carboncareasia.com/eng/Carbon_Solutions/Carbon_Calculators.php

- Carbon Footprint Ltd.: https://www.carbonfootprint.com/calculator.aspx

- Hong Kong Environment Bureau: https://www.carboncalculator.gov.hk/en

- The Nature Conservancy, USA: https://www.nature.org/en-us/get-involved/how-to-help/carbon-footprint-calculator/

- The Resurgence Trust: https://www.resurgence.org/resources/carbon-calculator.html

- USEPA: https://www3.epa.gov/carbon-footprint-calculator/

- WWF, UK: https://footprint.wwf.org.uk

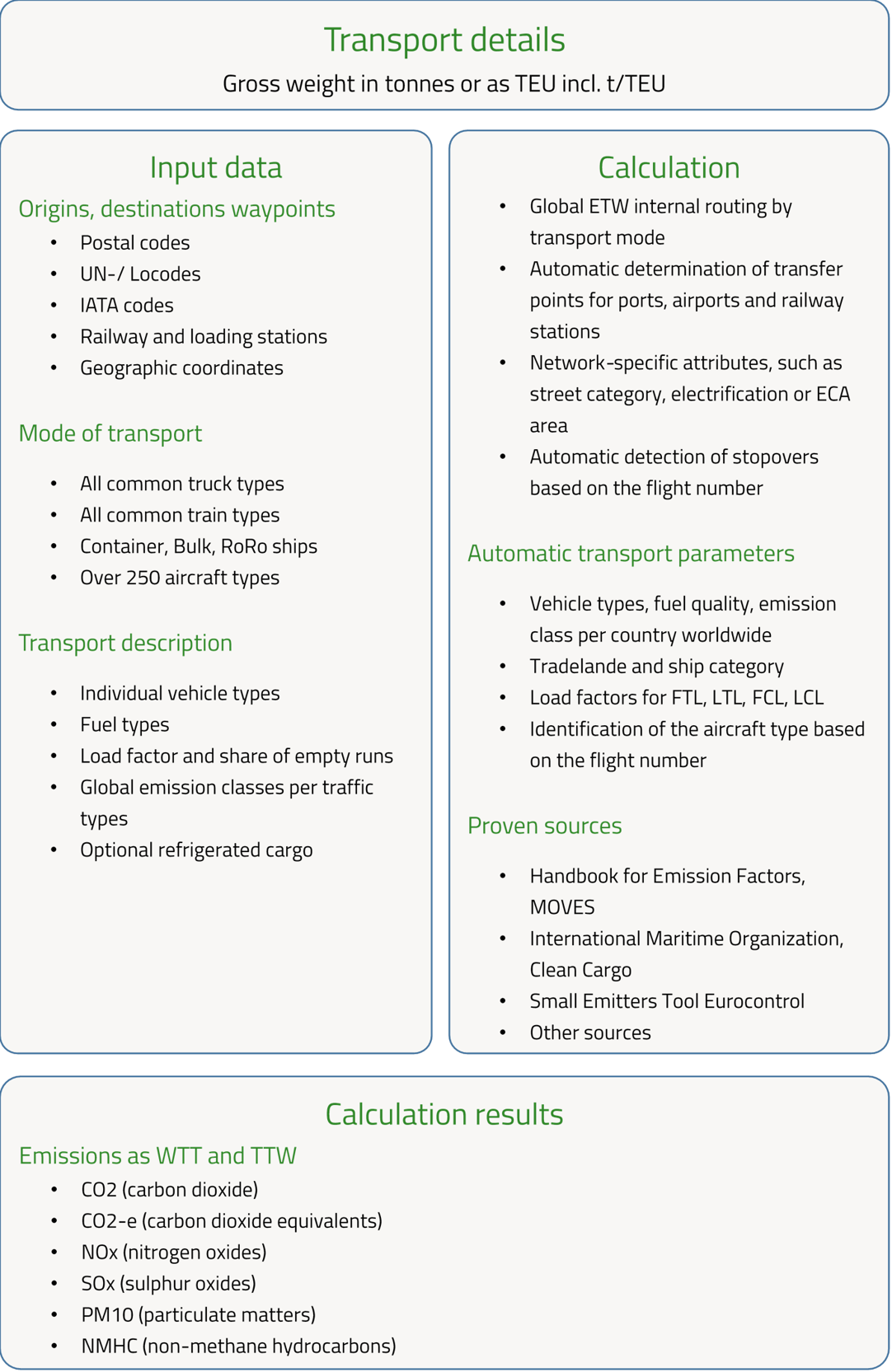

EcoTransIT World

Another carbon calculator is the EcoTransIT World. It is a very useful tool to calculate emissions caused from logistics activities, like transport, handling and storage. It is based on IPCC Assessment Reports about knowledge on climate change, its causes, potential impacts and response options and the ISO 14083 and the real data of companies. The figure "Structure of EcoTransIT" shows the different components of the tool. As a user, you need to insert the transport details (gross weight in tonnes or as TEU) and also other data like origins, destinations, waypoints, the mode of transport and a transport description. EcoTransIT is then doing the calculation by using automatic transport parameters from proven sources. It then gives the results for the different emissions for WTT and TTW.

The system covers the following information:

- Transport goods and volume

- Environmental parameters of each transport process

- Route characteristics and length

- Degree of capacity utilisation

- Vehicle size and drive type

Follow this link to test the EcoTransIT Calculator: https://emissioncalculator.ecotransit.world/

After calculating the emissions, the results must be documented in step 5.

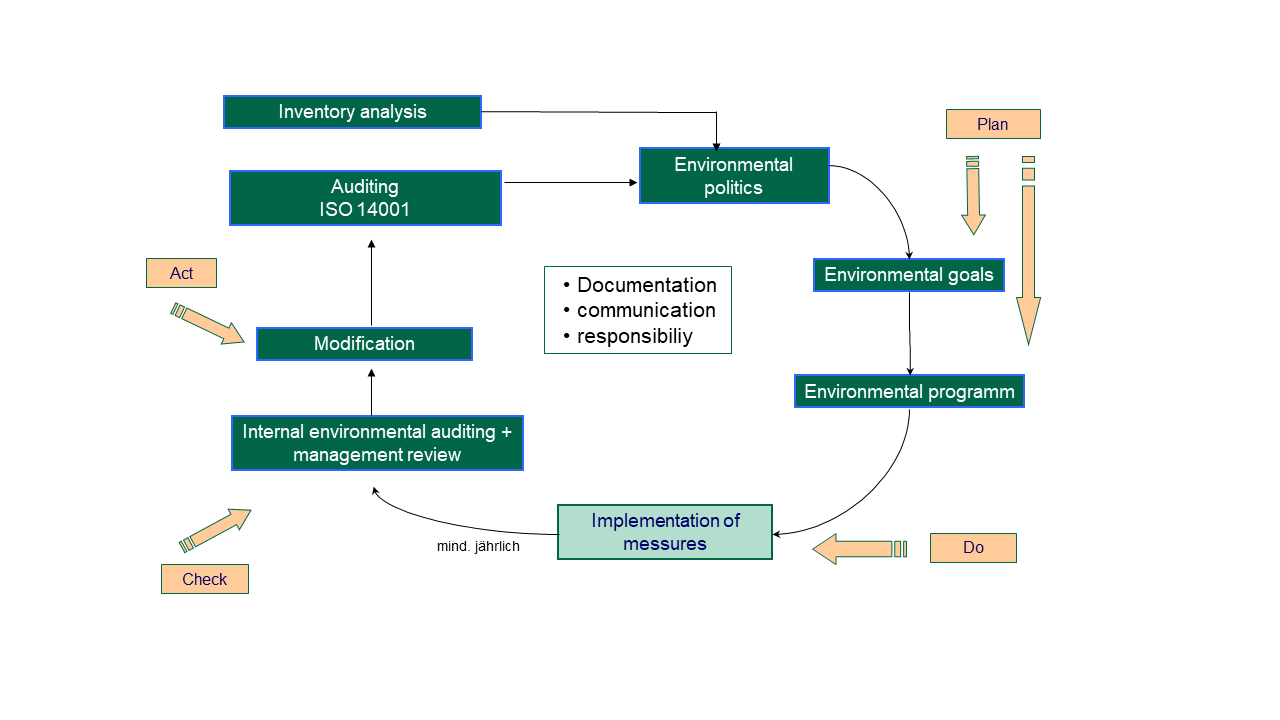

PDCA–Cycle (Plan Do Check Act)

To carry out the environmental analysis in accordance with ISO 14001 and ISO 14083 the PDCA-Cycle can be used. The PDCA Cycle describes an iterative four-phase problem-solving process that has its origins in quality assurance.

ISO 14001 focuses on a continuous improvement process as a means of achieving the defined objectives in relation to the environmental performance of an organisation (company, service provider, authority, etc.). The continuous improvement process is based on the Plan-Do-Check-Act (PDCA) method:

- Plan: defining the objectives and processes to achieve the implementation of the organisation's environmental policy

- Do: the implementation of the processes

- Check: Monitoring the processes with regard to legal and other requirements and objectives of the organisation's environmental policy; publishing the environmental performance (the organisation's success with regard to its environmental protection measures), if applicable

- Act: If necessary, the processes must be corrected (adapted)

The figure “PDCA-Cycle - Plan Do Check Act for environmental reporting” shows the different components, that need to be included when doing an environmental reporting.

The basis of the entire process is continuous documentation and communication and the clear definition of responsibilities for the planned measures and tasks.

In the case of environmental reporting, the environmental goals and programmes must be planned (Plan). The measures must then be implemented (Do), followed by an internal environmental audit and a management review at least once a year (Check). If the check shows that the measures are not effective, they must be changed (Act). The results are used for the ISO 14001 audit, which has an impact on the environmental policy. The environmental policy is also influenced by the status analysis and itself has an impact on the environmental goals.

Calculate the ecological and social impact

To evaluate whether a certain measure will be more ecologically friendly than another, you can use the following method to calculate CO2-emissions resulting from transport. The following figure "Determining ecological and social impacts and resource consumption and approaches for reducing transport-related environmental impacts" shows, how to calculate the ecological and social impact and resource consumption and how this consumption might be reduced.

With the multiplication of the transport distance [km] and the transport volume [t] you are able to calculate the tonne kilometres transported [TKT]. By multiplying the TKT with an emission factor (EF) [emissions/TKT] or with a consumption factor (CF) [resource/TKT] you can calculate the emissions [g] or the resource consumption [g]. The EF and the CF are dependent on the used mode of transport, so you need the vehicle miles travelled [VMT] to evaluate the whole ecological and social impact or resource consumption.

In transport, the main control variables are:

- the transport distance,

- the transported quantities (weight, volume) as well as

- the choice of the means of transport and

- its capacity utilisation.

Other important influencing factors are:

- the vehicle technology (e.g. type of means of transport, size, engine power, fuel used or traction type/energy mix and upstream chains),

- the operation (e.g. speed, driving behaviour, altitude) and

- the environmental and surrounding conditions (e.g. topography, flow conditions, weather).

For designing a more environmentally friendly product lifecycle, transportation is only one lever (keyword "local sourcing"). The sustainability of the freight transport depends mainly on the factors transport volume (weight, volume), transport distance, used mode(s), used concrete vessels and the degree of utilisation (load factor). To design a more environmentally friendly product life cycle in the area of transportation we should avoid transports (increase capacity utilization), shift transports (from road to rail), reduce speed (slow steaming), increase fuel quality (carbonization content in heavy fuel oil), etc. Both the shipper and the carrier can contribute to making transport more environmentally friendly with their decisions. The shipper can primarily influence the transport volume and distance, while the carrier can primarily influence the used mode and vessel as well as the load factor. The used mode of transport and load factor can also be influenced by the shipper if the shipper specifies which mode of transport is to be used and if the transport is only carried out when a sufficiently high load is available.

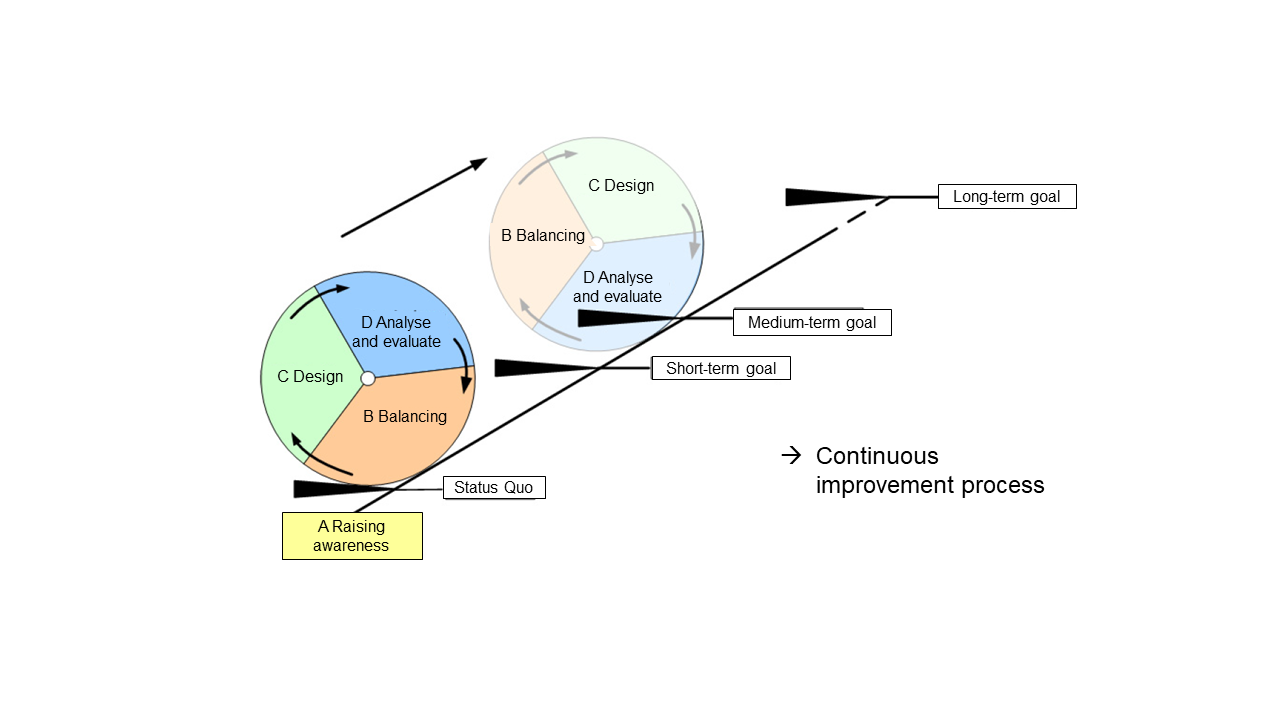

The following guidance can help companies if they want to reduce their GHG emissions from freight transport.

The first step (A) consists of raising awareness of the topic, whereby accountability must be institutionalised and targets formulated. The second step (B) involves balancing, where balancing limits need to be determined, prepared and implemented. The next step (C) involves designing, in which the reduction measures must be selected and implemented. The final step (D) involves analysing, evaluating and disseminating the results.

The process is continuously improved and steps B, C and D in particular are repeated again and again in order to achieve the short, medium and long-term goals.

The following figure “Guidance for companies on reducing transport related GHG emissions” shows the relevant aspects of raising awareness, balancing, design such as analyse and evaluate with respect to the level of goals in terms of short-term goals up to long-term goals. The repetition of the process and the individual steps depends on the desired goal and its temporal horizon.

You have now learnt more about the environmental dimension of sustainability and know how to calculate transport emissions. You have also gained an insight into who can take what steps to improve the sustainability of transport and how this improvement process can be organised. On the next page, you will learn more about the economic dimension of sustainability.

Sources

Bundesministerium für Umwelt, Naturschutz, nukleare Sicherheit und Verbraucherschutz (2024) Europäische Lieferkettenrichtlinie (CSDDD). URL: https://www.bmuv.de/themen/nachhaltigkeit/wirtschaft/lieferketten/europaeische-lieferkettenrichtlinie-csddd (last access: 06.06.2024)

Bundestag (2021): Act on Corporate Due Diligence Obligations in Supply Chains. URL: https://www.bmas.de/SharedDocs/Downloads/DE/Internationales/act-corporate-due-diligence-obligations-supply-chains.pdf?__blob=publicationFile&v=4 (last access: 06.06.2024)

Crippa, M., Guizzardi, D., Solazzo, E., Muntean, M., Schaaf, E., Monforti-Ferrario, F., Banja, M., Olivier, J.G.J., Grassi, G., Rossi, S., Vignati, E. (2021): GHG emissions of all world countries - 2021 Report, EUR 30831 EN, Publications Office of the European Union, Luxembourg, 2021, ISBN 978-92-76-41547-3

Deutschlandfunk (2022): Worum es bei der EU-Taxonomie geht https://www.deutschlandfunk.de/taxonomie-104.html (last access: 06.06.2024)

DIN EN ISO 14001:2015-11 (2015): Environmental management systems - Requirements with guidance for use

DIN EN ISO 14040:2021-02 (2021): Environmental management - Life cycle assessment - Principles and framework

DIN EN ISO 14044:2021-02 (2021): Environmental management - Life cycle assessment - Requirements and guidelines

DIN ISO 14083:2023-03 (2023): Treibhausgase - Quantifizierung und Berichterstattung über Treibhausgasemissionen von Transportvorgängen

EcoTransIT (2024): EcoTransIT World. URL: https://www.ecotransit.org/en/ (last access 24.05.2024).

EN 16258:2021 (2021): Methodology for calculation and declaration of energy consumption and GHG emissions of transport services (freight and passengers)

EN ISO 19011:2002 (2002): Guidelines for quality and/or environmental management systems auditing

European Commission (2022): DIRECTIVE OF THE EUROPEAN PARLIAMENT AND OF THE COUNCIL on Corporate Sustainability Due Diligence and amending Directive (EU) 2019/1937. URL: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX%3A52022PC0071 (last access: 06.06.2024)

EU Kommission (2022): EU-Taxonomie: Kommission legt ergänzenden delegierten Klima-Rechtsakt vor, um die Dekarbonisierung zu beschleunigen. URL: https://ec.europa.eu/commission/presscorner/detail/de/ip_22_711 (last access: 06.06.2024)

European Union (2022): Directive (EU) 2022/2464 of the European Parliament and of the Council of 14 December 2022 amending Regulation (EU) No 537/2014, Directive 2004/109/EC, Directive 2006/43/EC and Directive 2013/34/EU, as regards corporate sustainability reporting (Text with EEA relevance). URL: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:32022L2464 (last access: 06.06.2024)

Flämig et al. (2009): Die LOTUS-Methodik – Logistics towards Sustainability.

Flämig, H. (2015): Logistik und Nachhaltigkeit. In: Heidbrink, Ludger; Meyer, Nora; Reidel, Jo-hannes; Schmidt, Imke (Hrsg.): Corporate Social Responsibility in der Logistikbranche - An-forderungen an eine nachhaltige Unternehmensführung. Berlin: E. Schmidt, 2015. S. 25-44.

G8 Summit (2007): Climate Change, Energy Efficiency and Energy Security. Summit Declaration (7 June 2007). URL: https://www.g-8.de/Content/EN/Artikel/__g8-summit/anlagen/2007-06-07-gipfeldokument-wirtschaft-eng,templateId=raw,property=publicationFile.pdf/2007-06-07-gipfeldokument-wirtschaft-eng.pdf (last access 31.05.2024)

GHG Protocol (2011): Corporate Value Chain (Scope 3) Accounting and Reporting Standard. [online] https://ghgprotocol.org/sites/default/files/standards/Corporate-Value-Chain-Accounting-Reporing-Standard_041613_2.pdf (last access 13.06.2022).

GHG Protocol (2016): Global Warming Potential Values URL: https://www.ghgprotocol.org/sites/default/files/ghgp/Global-Warming-Potential-Values%20%28Feb%2016%202016%29_1.pdf (last access 31.05.2024)

GLEC Framework (2019): Global Logistics Emissions Council Framework for Logistics Emissions Accounting and Reporting. URL: https://www.feport.eu/images/downloads/glec-framework-20.pdf (last access 24.05.2024).

Greenhouse Gas Reduction Strategies in the Transport Sector (2008) - Preliminary Report; The International Transport Forum (ITF). URL: http://http://www.internationaltransportforum.org/Topics/CO2AbatementPDFs/WorldCO2.pdf

ISO 26000:2010-11 (2010): Guidance on social responsibility

McKinnon und Alan (2018): Decarbonizing logistics - distributing goods in a low-carbon world. URL: https://www.climatecouncil.ie/media/climatechangeadvisorycouncil/Transpor%20Transition%20Paper%202%20McKinnon%20Decarbonising%20Freight.pdf (last access 24.05.2024).

Mundancas Climaticas (2019): The Economics of Climate Change URL: http://mudancasclimaticas.cptec.inpe.br/~rmclima/pdfs/destaques/sternreview_report_complete.pdf, Part I-II (last access 13.06.2022).

Stern, N. (2006) Stern Review: The Economic of Climate Change.

URL: http://mudancasclimaticas.cptec.inpe.br/~rmclima/pdfs/destaques/sternreview_report_complete.pdf (last access 31.05.2024)

Umwelt Bundesamt (2022): Die Treibhausgase. URL: https://www.umweltbundesamt.de/themen/klima-energie/klimaschutz-energiepolitik-in-deutschland/treibhausgas-emissionen/die-treibhausgase#undefined, https://www.ghgprotocol.org/sites/default/files/ghgp/Global-Warming-Potential-Values%20%28Feb%2016%202016%29_1.pdf (last access 07.06.2024).

Umwelt Bundesamt (2022): Straßenverkehrslärm. URL: https://www.umweltbundesamt.de/themen/laerm/verkehrslaerm/strassenverkehrslaerm (last access: 31.05.2024)

Umwelt Bundesamt (2023): Umwelt und Verkehr. URL: https://www.umweltbundesamt.de/bild/infografik-umwelt-verkehr (last access 24.05.2024).

United Nations (2015): Paris Agreement. URL: https://unfccc.int/sites/default/files/english_paris_agreement.pdf (last access: 31.05.2024)

World Resources Institute and World Business Council for Sustainable Development (2004):

Greenhouse gas protocol, A corporate accounting and reporting standard. ISBN 1-56973-568-9. URL: https://ghgprotocol.org/sites/default/files/standards/ghg-protocol-revised.pdf (last access: 06.06.2024) .

Zhou (2020): Carbon Footprint Measurement. In: Carbon Management for a Sustainable Environment, pp 25-67.https://link.springer.com/content/pdf/10.1007%2F978-3-030-35062-8_2.pdf

4. Economic dimension

On the following page the economic dimension of sustainability will be explained to you. After showing you different providers of transport and logistics services, the transaction cost theory and the resource dependence theory will be explained.

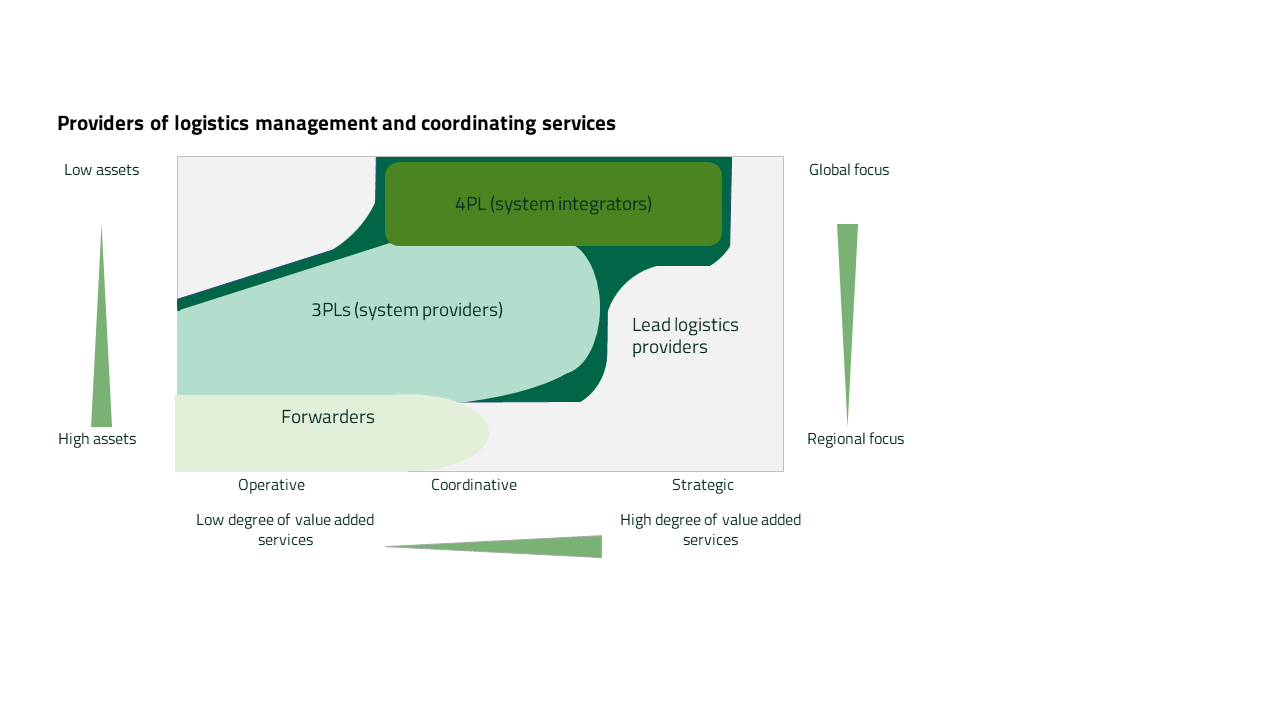

Types of logistics service providers

Logistics service providers are companies that provide logistics services for shippers, whereby the scope of the services provided differs. The following figure “Providers of logistics management and coordinating services” shows the differences between forwarder (2PL), third-party logistics provider (3PL), fourth-party logistics provider (4PL) and lead logistics provider (LLP). The 3PL are system providers, while the 4PL are system integrators. The actors differ in terms of their focus (global or regional), their amount of assets (low or high) and their coordinative (operative (low degree of value-added services) or strategic (high degree of value-added services)). While forwarders have high assets, a regional focus and a low degree of value-added services, the 4PL have low assets, a global focus and a high degree of value-added services.

A Forwarder (2PL) coordinates physical services of transport operators and other core logistics in integrated service package.

A Third-party logistics provider (3PL) operates large logistics networks by combining own and third-party logistics services and combines single services into customer-specific contract logistics service packages. Examples are door-to-door Supply Chains (SCs), complex storage tasks and value-added services as well as third-party Supply Chain Management (SCM)

A Fourth-party logistics provider (4PL) combines logistics services of 2PLs and 3PLs and provides related IT services. He acts on the logistics market without own physical assets.

A Lead logistics provider (LLP) integrates 3PL and 4PL services into LLP services and achieves additional added value by realizing process harmonization and providing a Supply Chain spanning IT-platform. Examples are the coordination of LSPs and suppliers in supply networks, merge-in-transit services, increased consolidation effects in awarding transport volumes to logistics providers, transparency and event-based disruption management.

The "physical" transport and logistics services can be provided by different actors, for example by:

- Container shipping lines

- Seaport terminal operators

- Inland transport operators (road, rail, barge)

- Inland terminal operators

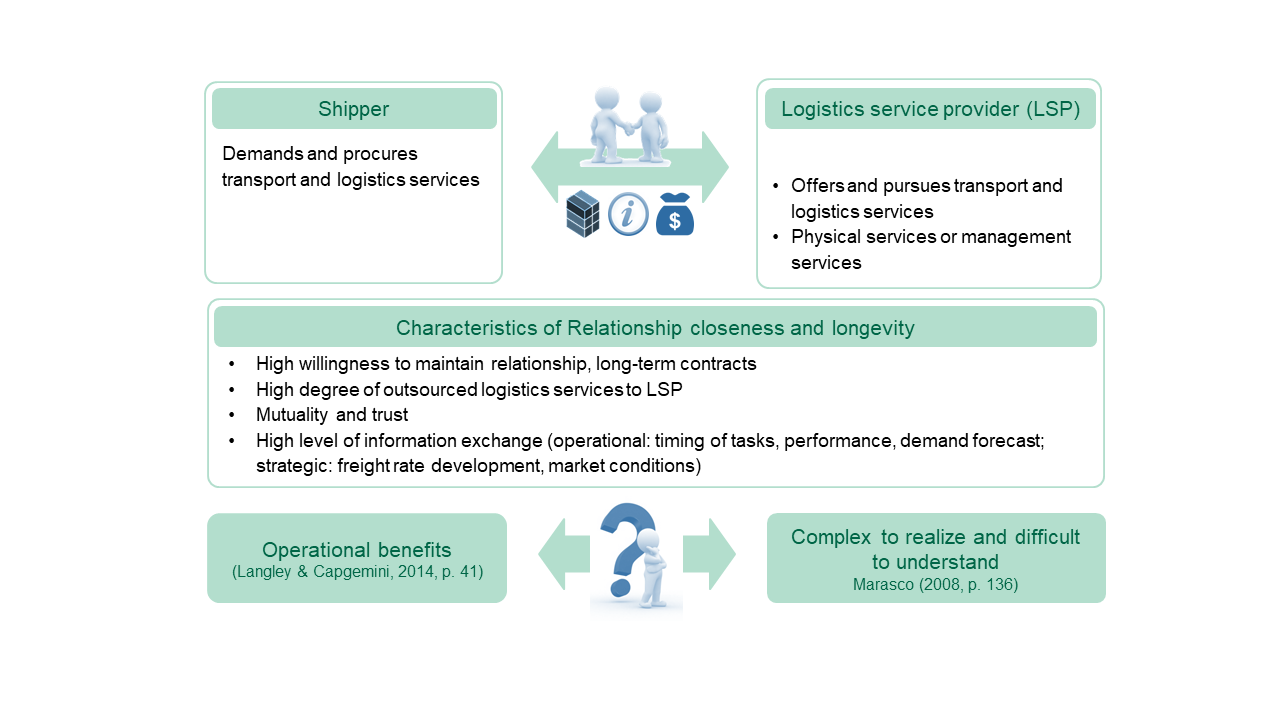

Close and Long-Term Shipper-Logistics Service Provider Relationships

The LSPs described above offer their services to shippers. “Shippers are business firms […] that utilize carriers for the transportation of goods from origin to destination locations.” Examples for shippers are e.g. cargo owners, firms who initiate the transport or to whom delivery is to be made and a shippers’ association. The contractual relationships between shippers and LSP vary and both short-term and long-term contracts are used. The following figure “Close and Long-Term Shipper-LSP Relationships” shows, what a long-term relationship means for the shipper and the LSP. It shows the responsibilities of the shipper (demands and procures transport and logistics services) and the LSP (offers and pursued transport and logistics services (physical or management)) and highlights, that this relationship is characterised by long-term contracts, a high degree of outsourced logistics services to LSP, mutuality and trust such as a high level of information exchange. While this agreement can lead to operational benefits, it is complex to realize and difficult to understand those kind of relationships.

The shipper and LSP have a commercial/contractual relationship and exchange information, cargo and/or financial flows. During the high level of information exchange both operational and strategic data are exchanged. At the operational level, data on the timing of tasks, performance and demand forecast is shared, at the strategic level, data on the freight rate development and market conditions is shared.

The "strong, lengthy and partner-focused relationships with their 3PLs and 4PLs" are needed by shippers "to attain more highly functioning and cost-effective supply chains" (Langley & Capgemini, 2014, p.41) but getting there might be difficult. “The path to achieving these results is not without its difficulties” and [i]mpediments are likely to be encountered in all the different phases of relationship development […].” (Marasco, 2008, p. 136)

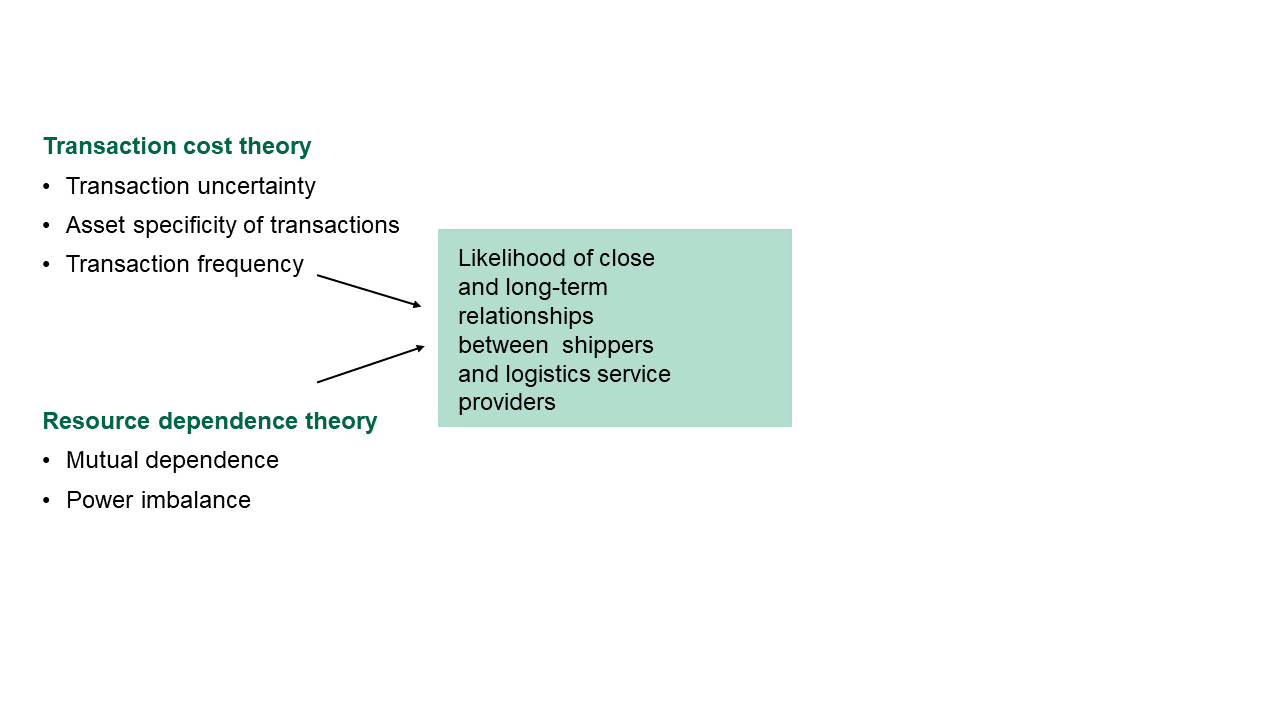

Causal model to explore shipper-LSP relationships

To understand the relationship between shippers and LSPs, a theoretical framework based on organisational theories can be used. This framework utilises transaction cost economics (TCE) and resource dependency theory (RDT). The following figure, "Causal model for analysing shipper-LSP relationships", shows how the two approaches can help determine the likelihood of close and long-term relationships between shippers and LSPs. Information on transaction uncertainty, asset specificity of transactions and transaction frequency is required from transaction cost theory, while results on interdependence and power imbalance are used from resource dependence theory.

The information on the six aspects is explained in detail in the following figure “Attributes of transaction cost economics and resource dependence theory”. While the TCE has an exchange perspective and all three constructs are having a positive influence on the likelihood of close and long-term relationship between shipper and LSP, the RDT has a resource perspective, where the resource and mutual dependence are having a positive association to the likelihood, while the power imbalance has a negative one.

Attributes of transaction cost economics and resource dependence theory, Source: Own figure (CC-BY-SA)

Transaction Cost Economics (TCE)

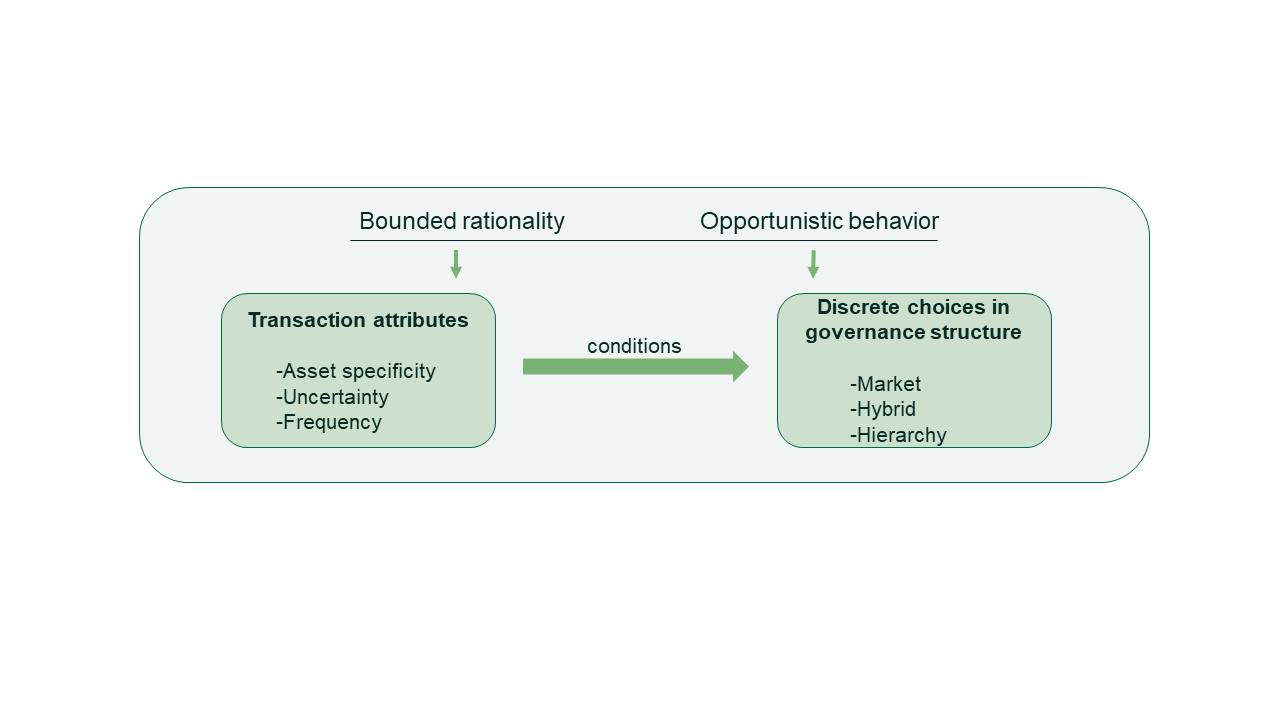

The TCE determines the most economical type of exchange relationship for each type of inter-firm exchange. The transaction cost theory by Williamson is defined as follows:

- “A transaction occurs when a good or service is transferred across a technologically separable interface” (Williamson, 1981, p. 552)

- TCE is widely used to determine ideal governance structures, that is, “the institutional framework in which the integrity of a transaction is […] decided” (Williamson, 1996, p. 11)

- “The overall object of the exercise essentially comes down to this: for each abstract description of a transaction, identify the most economical governance structure.” (Williamson, 1979, pp. 234-245)

The following figure „Components of transaction cost theory” shows the different transaction attributes (asset specificity, uncertainty and frequency) that are determining the discrete choices in governance structures between hierarchies, hybrid forms and markets. The key behavioral assumptions of the TCE are the bounded rationality and opportunistic behaviour. Because of the bounded rationality, actions might not be rational because of the limited capabilities to process and communicate information by the decision makers. The opportunistic behaviour assumes that "economic actors in contractual relations may take opportunities to dishonestly seek self-interest". This causes a behavioral uncertainty, as the economic actors can "not know, whether contracting parties behave opportunistically" (Herz 2015). The opportunism is more problematic, when the degree of asset specificity (degree to which an asset has a higher value to a specific relationship than outside the relational framework) is high, as the value of those assets is low outside of the relationship. A high asset specificity leads to high incentives to solve problems instead of ending the relationship. There are six types of asset specificity: equipment, site, human assets, facilities, timing of tasks and brand name.

TCE governance modes

There are three TCE governance modes (market, hybrid and hierarchy), that differ in terms of their degree of relationship intensity. While the market governance mode has the lowest relationship intensity, the hierarchy governance mode has the highest. The three governance modes have the following specifications:Market governance

- Recurrent transactions via the market, identity of exchange partners is not important.

- Buyers and suppliers respond to price changes. They decide autonomously to either switch (for little costs) or maintain exchange.

Hybrid governance

- The Identity becomes important. The value of specific assets is closely connected to transaction partner

- Mutual consent needed to react to disturbances (cooperation)

- Legal autonomy of partners is maintained

Hierarchy

- Vertical integration: adaptation by goodwill without interference of other parties

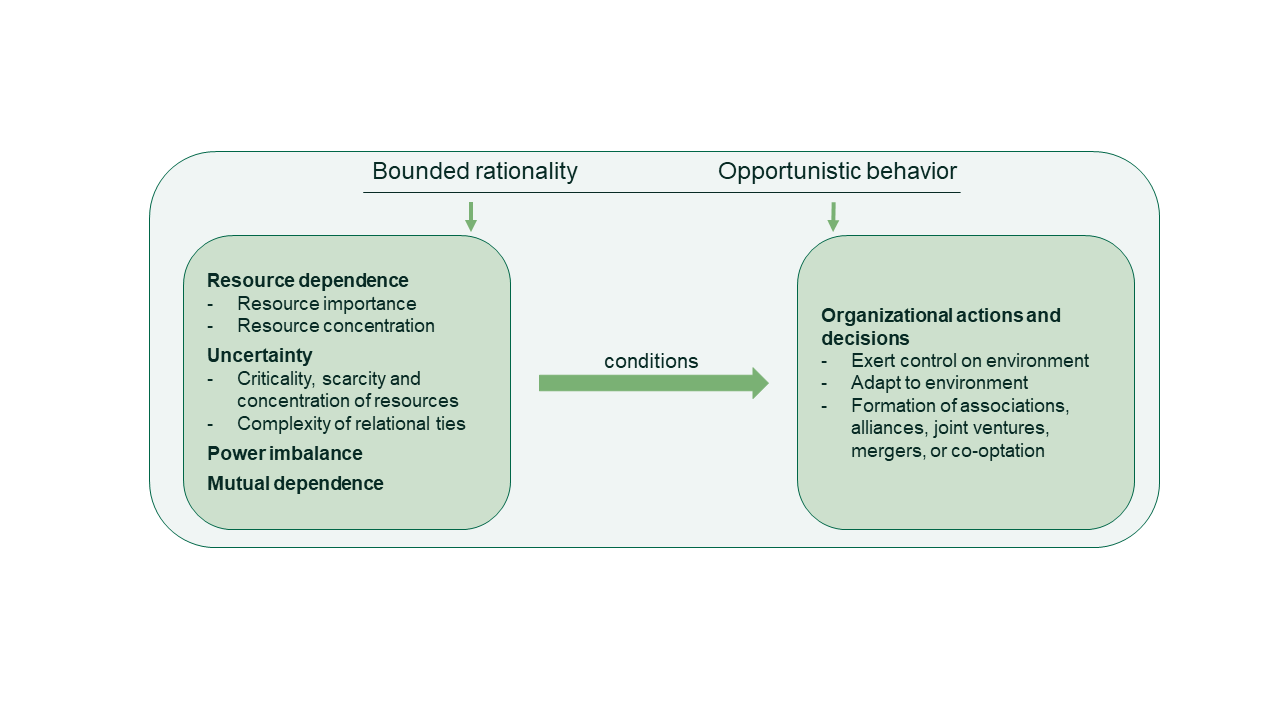

Resource Dependence Theory (RDT)

The RDT is used to build close relationships with exchange partners that allow you to minimize resource dependence. It explores how dependence on external resources affects the distribution of power between actors and ultimately influences its relationship. It also includes the role of environmental contingencies in inter-organisational relationships.

The following figure “Components of resource dependence theory” shows the behavioral assumptions, components (resource dependence (resource importance, resource concentration), uncertainty (criticality, scarcity and concentration of resources, complexity of relational ties), power imbalance and mutual dependence) and the proposed relations of the RDT. The four components are determining the organisational actions and decisions like exert control on environment, adapt to environment and the formation of associations, alliances, joint ventures, mergers or co-optation. Like the TCE, the key behavioral assumptions of the RDT are the bounded rationality and opportunistic behaviour.

RDT Governance modes

There are different strategies to regulate relations with your partners. You should “Choose the least-constraining device to govern relations with your exchange partners that will allow you to minimize uncertainty and dependence and maximize your autonomy” (Davis & Cobb 2006, p. 24). Some tactics forego direct involvement of those who exert dependence, so that organizations adapt to their environment (sourcing diversification, increase firm size). Other strategies directly target the nature of the inter-organizational relationship between dependent parties in order to manage interdependencies and reduce power imbalances and to improve control over strategic resources (alliances, joint ventures, mergers).

Location and Accessibility Matter – Spatial Concentration of Services Creates Lock-In for Shippers

Not only are the LSPs dependent on the shippers, but the shippers can also be dependent on the LSPs. The following figure “Spatial Concentration of Services Creates Lock-In for Shippers” shows a centralisation of a supply network in 2002, which led to a spatial consolidation of goods flows. In this example, the LSP operates the central warehouse and the port on-carriage. This leads to operational advantages for goods inflow (economies of scale, sustainability targets) and goods outflow (increased flexibility through consolidated flows) but creates a high level of dependency for the shipper that is difficult to reverse. The spatial concentration of supply network, location and accessibility of LSP facilities strongly influences shippers’ decisions to engage with and maintain relationships with LSPs.

There exists a close proximity between the trimodal accessible LSP’s facilities and seaports further logistics sites that enables shippers:

- to use mass compatible modes of transport,

- to realize economies of scale in transportation and goods handling,

- to increase operational flexibility by keeping flows consolidated as long as possible.

The shipper-LSP exchange is influenced by the site specific nature of the logistics services pursued and hence depended on the spatial organization of the supply network as a whole. So, in all cases shippers improved SC efficiency and flexibility by keeping flows consolidated as long as possible and by utilizing the close proximity between LSP-operated logistics facilities, seaports and additional logistics sites.

Summary

- Stable and predictable earnings

- Learning effects and know-how development from long-term contract logistics deals to strategically grow in certain logistics fields → reduce cyclicality of business

- Cross-fertilization of other business segments such as port logistics

- Safeguards to reduce own investments in facilities and equipment

- Improved ability to outsource ever larger, more complex and sophisticated logistics tasks

- Realize economies of scale

- Access to LSP’s innovative capacity or to relationship-specific knowledge

- Avoidance of own investment in physical assets

- Secure access to certain valuable resources in the long run that brings certain operational benefits like:

- Logistics services that meet certain quality criteria (e.g. reliability, responsiveness, asset utilization)

- Services provided at concrete locations or guarantee access to certain facilities

- Services that allow to make use of specific transport operators or mass-compatible modes of transport

- Superior information management services

Sources:

Drees & Heugens (2013). Synthesizing and extending resource dependence theory: A meta-analysis. Journal of Management, 39(6), 1666–1698. https://doi.org/10.1177/0149206312471391

Herz (2015): Understanding close and long-term relationships between shippers and logistics service providers: A case-based analysis of their determinants and their implications for transaction cost economics and resource dependence theory. Dissertation.

Langley, John, JR.; Capgemini (2014): 2014 Third-party logistics study: The State of Logistics Outsourcing. Results and Findings of the 18th Annual Study. Available online at http://www.capgemini.com/resource-file-access/resource/pdf/3pl_study_report_web_version.pdf (last access 23.12.2014).

Marasco, Alessandra (2008): Third-party logistics: A literature review. In International Journal of Production Economics 113 (1), pp. 127–147.

Talley, W.K. (2009): Port Economics (1st ed.). Routledge. https://doi.org/10.4324/9780203880067

Teece, David J. (1986): Transactions cost economics and the multinational enterprise: An Assessment. In Journal of Economic Behavior & Organization 7 (1), pp. 21–45

United States Congress (1984): Shipping Act of 1984 - An Act to improve the international ocean commerce transportation system of the United States. STAT. 67 Public Law 98-237

Williamson, Oliver E. (1979): Transaction-Cost Economics: The Governance of Contractual Relations. In Journal of Law and Economics 22 (2), pp. 233–261.

Williamson, Oliver E. (1981): The Economics of Organization: The Transaction Cost Approach. In American Journal of Sociology 87 (3), pp. 548–577.

Williamson, Oliver E. (1996): The Mechanisms of Governance. 1st ed. New York: Oxford University Press.

Walker & Weber (1984): A Transaction Cost Approach to Make-or-Buy Decisions. Administrative Science Quarterly, Vol. 29, No. 3. (Sep., 1984), pp. 373-391.

4.1. Quiz - Economic dimension

Check your knowledge on the economic dimension with the following quiz.

5. Sustainability in the Conceptual System Model of Transport and Traffic

The following page explains you why logistics needs to become more sustainable and what measures can be taken to make the elements and relationships of the conceptual system model of transport and traffic more sustainable.

The reliability of (not only) global supply chains is severely jeopardised by climatic events. Trains and trucks are prevented from continuing their journeys by freezing rain or snow. Transport by water is not possible all year round or only at reduced speed or capacity. Due to water level fluctuations, especially in the free-flowing sections of the rivers caused by precipitation and melting snow, ships cannot travel all year round. When the water level is low, the ships have a too great draught and therefore cannot use the waterways. If the water level is too high, the ships cannot pass the bridges as they are not high enough.

The survival of companies from an economic perspective depends on a variety of framework conditions. From the marketing side, it is primarily the customers who determine the future of the companies. Hence, companies are analyzing what influences customers in their purchasing decisions and figuring out their sustainability mindset. At the same time, however, the political framework conditions are placing even greater demands on companies to operate in a sustainable manner. Competitors are also adapting to this, so that their activities also represent benchmarks for the own company. Benchmarks of companies are also used by financiers and insurers of the companies, which are becoming increasingly important.

Sustainability in the Conceptual System Model of Transport and Traffic

In order to make the goods movement more sustainable, different measures can be taken by different stakeholders. The following figure “Measures to improve the sustainability of goods movement” shows, which different measures can make the elements and relations more sustainable, thereby increasing the sustainability of the entire system.

Now you should know more about the various measures that can help improve the sustainability of goods transport. You can test your new knowledge on the next page.

Sources

Antonio Marco (2024): Neue Trends in der internationalen Logistik: Herausforderungen und Chancen. URL: https://antoniomarco.com/news/de/neue-trends-in-der-internationalen-logistik-herausforderungen-und-chancen/ (last access 27.05.2024).

AMS (2024): Green Warehouse: The Eco-Friendly Warehousing. URL: https://www.amsc-usa.com/blog/green-warehouse-sustainable-logistics/ (last access 24.05.2024).

Fraunhofer (2021): Micro-Hubs für eine nachhaltige Citylogistik. URL: https://www.stuttgart.de/medien/ibs/micro-hubs-fuer-eine-nachhaltige-citylogistik-final.pdf (last access 24.05.2024).